Note

3/4/2020: Rewritten in English.

24/12/2014: Moved from wiki.

Generally

- The principle and practice described below is based on the Standard Forms of Building Contracts Private Editions. The Government General Conditions of Contract are similar. The contract prices are generally fixed as lump sums or unit rates as tendered for at the risks of the Contractor, and will not be changed except for specified circumstances.

- However, the principle and practice used in the family of New Engineering Contract are very different. The core concept is to remove the risk of the Contractor in pricing. The costs are generally reimbursed based on the final quantities carried out and the actual costs paid by the Contractor, with a percentage addition for the Contractor's fees which should cover his profit and overheads not within the definition of "costs".

Preparing Final Accounts and negotiating with the contractors to agree the Final Accounts

- The Final Account process should start as and when a variation instruction is issued and should not be deferred until after Substantial / Practical Completion.

- Any update should be reflected in the Financial Reports.

- The Financial Reports with the column for the amounts estimated by the QS can be issued to the Contractor so as to present a full picture of his claims and QS’s assessment, and more importantly the areas of major differences for priority treatment.

- Upon the agreement of the Final Contract Sum, the Financial Reports can be converted to formal Final Account format for signing.

- The key difference is that the Final Account only needs to show the amounts agreed and usually the gross omissions and gross additions are shown in two columns, while the Financial Reports show more columns as mentioned above, and due to limitation of page width, only a single column for the nett amounts is shown.

Descriptions

- The description of the items in the Financial Reports (to be converted to Final Account) should concisely but properly represent the design change or the scope of the costs.

- Do not copy directly from the description in the Architect’s instruction.

- Traditionally, the descriptions are written in instructive sense meaning the Contractor has to do it, such as:

- Add a concrete plinth at plant room A.

- However, if the Architect’s instruction says “BD general plan amendment submissions are hereby issued for your reference”, then a Financial Report description like the following would not be appropriate:

- Issue BD general plan amendment submissions for reference.

- A more proper description would be:

- Receive BD general plan amendment submissions for reference.

- Therefore, instead of writing in instructive sense, the following neutral style would be more appropriate:

- Addition of a concrete plinth at plant room A.

- Issuance of BD general plan amendment submissions for reference.

Main items adjusting Contract Sums

- Variations.

- Adjustment of prime cost rates.

- Adjustment of provisional quantities.

- Adjustment of daywork allowances.

- Adjustment of Provisional Sums (including Contingency Sum).

- Adjustment of Prime Cost Sums and related profits.

- Loss and expense due to disruptions and delays.

- Adjustment for cost fluctuations.

- Others adjustments such as:

- deduction in lieu of correction of errors in setting out the Works

- deduction in lieu of replacement or reconstruction of materials, goods or work that are not conforming

- deduction in lieu of rectifying defects

- addition of statutory fees and charges which are additional to the Contractor's responsibilities

- opening up and testing materials, goods or work which are additional to the Contractors' responsibilities and complying with the Contract

- effecting and maintaining insurances resulting from the Employer’s failure to insure.

Authority

- Except for loss and expense claims and adjustments for cost fluctuations, Architect’s Instructions are required to authorize the work carried out under other items causing cost additions.

- Loss and expense claims do not necessarily arise due to Architect’s Instructions.

- The rules for adjustments for cost fluctuations must have been detailed in the Contract and would not need Architect’s Instructions.

- Provisional quantities by default must be adjusted for the final quantities done with authorization. The authorization may be in the form of the work being shown on drawings issued for general construction. Therefore, arguably, specific Architect’s Instructions may not be required.

- Excessive work done not as instructed will not be entitled to payment even though it may be tolerated without removal.

Abortive work and daywork records

- Abortive work and daywork must be properly recorded by the Contractor with photos, dimensioned measurement details, quantities of labour employed, materials used, plant used, etc.

- Endorsement by the Clerk of Works or the Architect’s / Engineer’s site representatives is required.

- In case no endorsement is available, the Architect’s opinion should be sought.

- Payments made by the Contractor must be supported by invoices and receipts issued by the sub-contractors or suppliers.

Work not done

- Work not done but not yet omitted by an Architect’s Instruction should not be included in interim payment.

- Its omission value should be noted in the Financial Reports to ensure that this would not be missed in the Final Account.

- If eventually the work is not done, the value should be omitted from the Final Account for agreement without necessarily requiring an Architect’s Instruction.

Filing

- The documents relating to the above different items should be filed under different files.

- Architect’s instructions should each be filed under a different file section such that the instruction is put at the front of its section while other documents from estimates before AI, AI pre-approval form, Contractor’s submissions, QS assessment, etc. are filed in chronological order with the latest put on top. This would serve to tell the full history of development.

Drawing register

- For big projects, the Drawing Register used in the Pre-contract stage can continue to be updated, but with the Architect’s Instruction Numbers added at the column headers.

- The Drawing Register can reveal whether a drawing has been revised several times under different Architect’s Instructions.

- It is more efficient to measure the final change against the original instead of measuring changes after changes.

Rates to be used

- Rates used to value variation additions, remeasured provisional quantities and expenditure of provisional sums:

- Contract rates - for work of similar character carried out under similar conditions

- Pro-rata rates - based on contract rates for similar work but adjusted for the differences in character or conditions of work

- Fair market rates - used if it is unreasonable to apply contract rates or pro-rata rates, e.g. work is entirely different

- with reference to similar work in other projects and adjusting for the differences between the two projects

- build-up from first principle

- Daywork rates - to be used when it is unreasonable to measure and value the work based on the quantity of the work, e.g. in case of demolition, piecemeal breaking up of openings.

- Rates used to value variation omissions and omission of original provisional quantities

- Contract rates - for omission of quantities of original work

- Pro-rata rates - if the reduction in the quantities is significant and renders the contract rates for the remaining quantities unreasonable to apply, then the rates for the remaining quantities can be adjusted for the cost differences caused by that reduction. An example is a change in the economy of scale. The contract rates have to share some fixed costs based on the original quantities. If the quantities are reduced significantly, the fixed costs contributed by the remaining quantity will not be sufficient. An adjustment should be made to the contract rate to compensate the contribution so lost.

High or low contract rates

- Contract rates are to be applied no matter whether they are high or low. The same principle applies to adjusting contract rates for pro-rata rates. The adjustment should be for the cost difference between the differences in character or conditions or economy of scale.

Omission and addition

- Generally, when a drawing is revised, the quantities of the items changed are measured as omissions, and the quantities of the items after change are measured as additions.

- However, if only the component design is changed but the quantity remains the same, then it should be more expedient just to apply the rate difference to the quantity to give the net adjustment.

Variations

- The 2005/2006 versions of the Standard Forms of Building Contract define variations as:

Variation: a change instructed by the Architect to the design, quality or quantity of the Works including:

(i) an alteration to the type, standard or quality of any of the materials or goods comprising the Works;

(ii) the addition, substitution or omission of work; and

(iii) the removal from the Site of materials or goods and the demolition and removal of work except where provided for in the Contract or where the materials, goods or work are not in accordance with the contract clause regarding types, standards and quality;

or the imposition of an obligation or restriction instructed by the Architect regarding:

(iv) access to the Site or use of any parts of the Site;

(v) limitation of working space;

(vi) limitation of working hours; or

(vii) the sequence of carrying out or completing work;

or the addition or alteration to or omission of such obligations or restrictions imposed by the Contract.

- The Government General Conditions of Contract are very similar.

- The pre-2005/2006 versions of the Standard Forms of Building Contract do not have scope similar to (iv) to (vii).

- The Architect Instruction number must be stated to indicate the authority.

Errors

- Errors in Tender Documents forming part of the Contract Documents are to be corrected for carrying out the work and the cost effects are to be treated as variations.

- Architect’s Instructions would usually be issued to make the corrections of errors in the Drawings and Specification without being explicit of being an error correction.

- No Architect’s Instruction is required for correction of BQ errors, and the correction is deemed to be a variation. However, the presence of BQ errors would not give a good image of the QS to the Client. If it so happens that the BQ items with errors are also subject to design change, then it is not uncommon that the correction of BQ errors will be made when valuing the design change.

- Errors in the Contractor's pricing of the Tender Documents are not to affect the Contract Sum.

Adjustment of prime cost rates

- The Final Account adjustment items would be like:

- Omission of original quantity x prime cost rate = gross omission

- Addition of original quantity x actual unit cost = gross addition

- Alternatively

- Original quantity x (actual unit cost - prime cost rate) = net adjustment

- The BQ reference should be stated.

- Where available, state also the Architect Instruction number.

- Usually, the Contract specifies that no adjustment will be made for wastage or profit and overheads.

- However, if the actual unit cost is excessively more than the prime cost rate, the Contractor will suffer in the wastage cost with insufficient profit and overheads. A reasonable compensation of the excessive effects of the wastage and profit and overheads should be made.

- On the other hand, there can be savings in other items where the actual unit costs are less than their prime cost rates.

- Therefore, the reasonable compensation should then take a global view considering all prime cost rate adjustments.

- The all-in rate after adjusting the prime cost rate for the actual unit cost is as follows:

- Original all-in rate – prime cost rate + actual unit cost = adjusted all-in rate

- The adjusted all-in rates should be applied to changes to the original quantity due to variations whether it be omission or addition.

- If the original all-in rates are consistently used for valuing variations, then the adjustment of prime cost rates should be based on the final quantities inclusive of all variations.

- The materials or work covered by the prime cost rates require specific selection and approval by the Architect, therefore, the actual unit cost should be part of his consideration and the Architect’s Instruction confirming the selection should state the actual unit cost approved.

- However, there may be cases that this process is overlooked or the selection is just left to the Contractor who submit the actual unit cost information after carrying out the work.

- In this case, the actual receipt of money paid must be submitted. Quotations and invoices can all be subject to changes. Receipts may also be forged, but this is a criminal offence.

Adjustment of provisional quantities

- The Final Account adjustment is in the form of remeasurement with items like:

- Omission of original quantity x original rate = gross omission

- Addition of final quantity x original rate = gross addition

- The BQ reference should be stated.

- Where available, state also the Architect Instruction numbers.

- The final quantities should be measured based on the final set of drawings issued under Architect’s Instructions for construction.

- It is not necessary that the Architect’s Instruction specifically states that the drawings are for the purpose of remeasurement.

- While it is time saving to measure based on the final set of drawings, it may mean to happen at a very late stage of construction leaving no realistic amounts for payment valuation and financial reporting.

- Therefore, it is also possible to measure based on a comprehensive set of drawings in the early stage and treat all subject changes as variations.

- It is possible than the design of the original provisional quantities has been changed but the nature remains the same, for example, provisional quantities have been included in the Contract for the components making up composite items, but the component sizes have been changed. Therefore, pro-rata rates have to be valued for the varied component. It should be acceptable to include the varied components at pro-rata rates in the adjustment of provisional quantities rather than treating them artificially as variation items.

Adjustment of daywork allowances

- A daywork schedule included in the BQ usually contains the following:

- Daily or hourly labour rates inclusive of profit and overheads

- Daily or hourly plant rates inclusive of profit and overheads

- Provisional Sums for materials with priced % mark-up for profit

- If the BQ includes a daywork schedule, the Final Account adjustment items will be like:

- Omission of total of daywork schedule

- The BQ number should be stated.

- The additions for expenditure based on daywork rates should be reflected in the relevant variations instead of being shown here.

- The quantities of labour, materials and plant used must be endorsed by the Clerk of Works or the Architect’s or Engineer’s site representative, failing which, the Architect.

- Difficulties can arise as to how to count the lunch hours and recess minutes.

- The quantities of materials can include wastage.

- The priced labour rates and plant rates are to be used

- The material costs must be evidenced by receipts issued by the suppliers, with an addition for profit based on the priced % mark-up.

Adjustment of Provisional Sums (including Contingency Sum)

- The Final Account adjustment items will be like:

- Omission of provisional sum for some work

- Addition of work at room A

- Addition of work at room B

- The BQ reference should be stated for the omission.

- The Architect’s Instruction numbers should be stated for the additions.

- The backup calculations for the addition should be in the form of quantities x rates.

- It is usual to omit the Contingency Sum first in the Final Statement, and show the adjustment of other Provisional Sums separately in a later section.

Adjustment of Prime Cost Sums and related profits

- The Final Account adjustment items will be like:

- Omission of prime cost sum for Lift Nominated Sub-Contract Works

- Omission of profit at %

- Omission of attendance

- Addition of Final Sub-Contract Sum for Lift Nominated Sub-Contract Works

- Addition of profit at %

- Addition of attendance

- The BQ reference should be stated for the omission.

- The Architect’s Instruction numbers nominating the Sub-Contractor should be stated for the additions.

- The price for attendance should be treated as lump sums and not to be adjusted.

- However, if because of a significant change of the scope of the Sub-Contract Works resulting in different scope of attendance, then adjustment of the attendance would need to be made.

Adjustment of Nominated Sub-Contract or Supply Contract Sums

- The original Nominated Sub-Contract or Supply Contract Sums are also subject to adjustments for variations, provisional quantities, etc. as described above. A separate Final Account should be prepared for each of them.

- The Final Sub-Contract Sum or Supply Contract Sums are then brought forward to the adjustment of Prime Cost Sums.

Loss and expense due to disruptions and delays

- Loss and expense claims arise when the normal valuation cannot cover the Contractor’s costs.

- Loss and expense due to variations (e.g. late additional order due to late instructions, reduced quantity after ordering, late instruction after the bulk of work has been completed) should be dealt with under the variations as much as possible, except when they involve compensation related to disruption to the regular progress of the relevant work (with or without variation change in quantities) or prolongation of the Contract Period.

- Loss and expense due to disruptions and delays are permissible if the event causing the disruptions and delays are compensable events under the Contract.

- The 2005/2006 versions of the Standard Forms of Building Contract allow compensation of loss and expense due to the following events (“qualifying events”):

- an Architect's instruction to resolve an ambiguity, discrepancy in or divergence between the documents listed in that clause

- an Architect's instruction requiring the opening up for inspection of work covered up or the testing of materials, goods or work and the consequential making good where the cost of such opening up, testing and making good is required by that clause to be added to the Contract Sum

- an Architect's instruction requiring a Variation

- an Architect’s instruction resulting in an increase in the work to be carried out of sufficient magnitude to cause delay or disruption, provided that the variance was not apparent from the Contract Drawings

- an Architect's instruction regarding:

- the postponement of the Date for Possession of the Site or a part of the Site

- the postponement of the Commencement Date of the whole or a part of the Works; or

- the postponement or suspension of the whole or a part of the Works, unless:

- notice of the postponement or suspension is given in the Contract; or

- the postponement or suspension was caused by a breach of contract or other default by the Contractor or any person for whom the Contractor is responsible

- compliance with contract clause regarding preservation of an object of antiquity or with an Architect’s instruction requiring the Contractor to permit the examination, excavation or removal by a third party of an object of antiquity found on the Site

- late instructions from the Architect, including those to expend a Prime Cost Sum or a Provisional Sum, or the late issue of the drawings, details, descriptive schedules or other similar documents, except to the extent that the Contractor failed to inform the Architect sufficiently in advance of the time that he requires the supplementary information

- delay or disruption caused by a sub-contractor or supplier nominated by the Architect despite the Contractor’s valid objection to the extent that the delay or disruption was attributable to the grounds for objection raised by the Contractor to the nomination of the sub-contractor or supplier

- delay or disruption caused by a Specialist Contractor

- the failure of the Employer to supply or supply on time materials, goods, plant or equipment that he agreed to provide for the Works

- the failure of the Employer to give possession of the Site or a part of the Site on the agreed Date for Possession of the Site or the part of the Site, or subsequently the Employer depriving the Contractor of the whole or a part of the Site

- any other delay or disruption for which the Employer is responsible including an act of prevention or a breach of contract.

- It should be noted that neutral events (i.e. events neither caused by the Employer nor the Contractor nor persons for whom they are responsible) do not have financial compensation. Only a restricted number of neutral events has extension of time.

- The usual heads of claims are:

- Loss of productivity

- Inflationary increase

- Running site overheads (longer time to employ, engage, hire, maintain, repair)

- Site management team (site based on head office based)

- Site levellers

- General support labour

- Security guards

- Site construction plant like tower cranes, hoists, lifts

- Temporary site facilities like site offices, workshops, stores, water, electricity

- Extension of insurances and bond

- Running head office overheads

- Head office rental, management fees, rates, air-conditioning charges, office appliances, water, electricity, telephone, internet, stationery, sundry expenses

- Head office management and support staff

- Finance charge on additional costs

- Loss of profit otherwise recoverable had there been no delay

- Compensation of loss and expense is based on the difference between the costs incurred after the qualifying event as compared to those which would have been incurred without the event causing the event.

- Site overheads are mostly priced in the preliminaries, but the preliminaries prices can be higher or lower than the costs which would have been incurred without the event. Therefore, the preliminaries prices would not be used to calculate the loss and expense. However, for quick estimate, people do use the running part of the preliminaries price per day to estimate the loss and expense per day for budgetary purposes. If the preliminaries price is not out of order, people may as well settle the site overheads compensation based on the running part of the preliminaries price per day x the number of days prolonged.

- When the Contractor price for the head office overheads, he would estimate a lump sum or a percentage mark-up on the costs to cover his head office overheads. That percentage mark-up may be based on his company’s annual head office overheads / annual site cost. If the Contract is prolonged, the same head office overheads have to be recovered over a longer period of time, and the percentage mark-up has become less, and the Contractor will suffer loss unless he can earn more head office overheads from other projects. However, as far as this project is concerned, because the project team is engaged for a longer time to deprive the Contractor to use the same team to earn head office overheads from other projects, compensation for the under-recovery of head office overheads should be given.

Final Account format

-

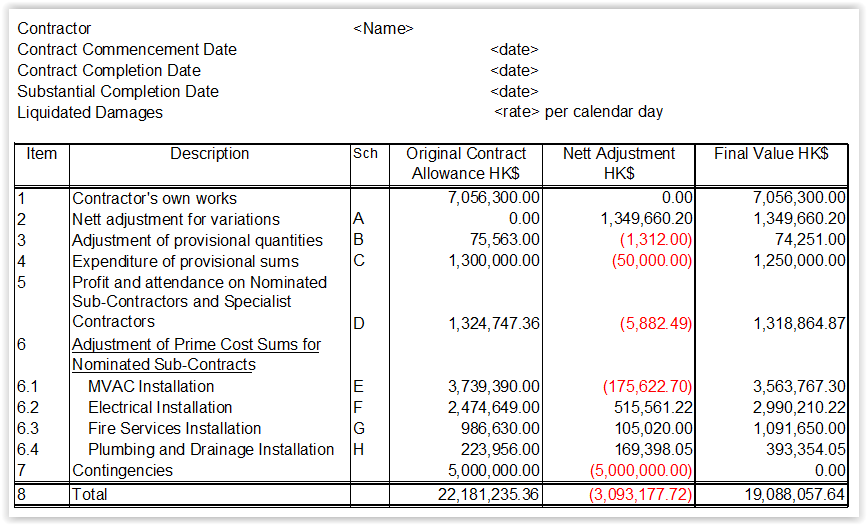

A summary of the Final Account may look like this:

-

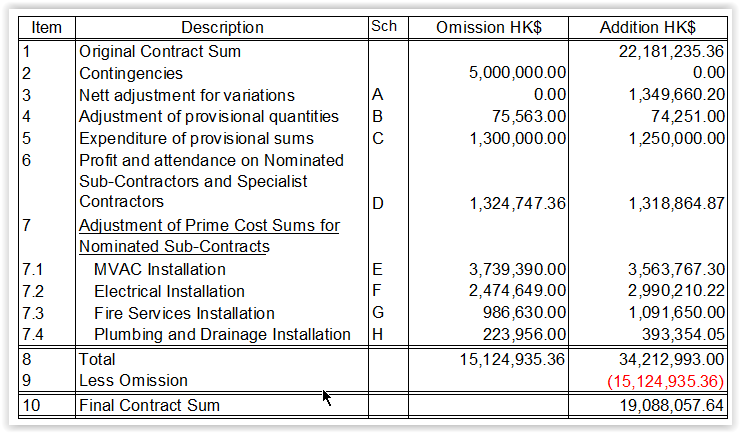

Most Consultant QS firms use two columns only like this:

-

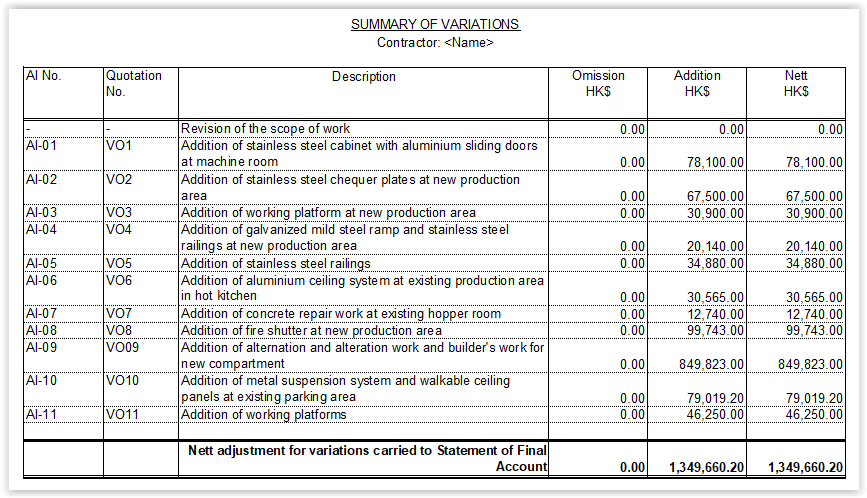

A Summary of Variations may look like this:

-

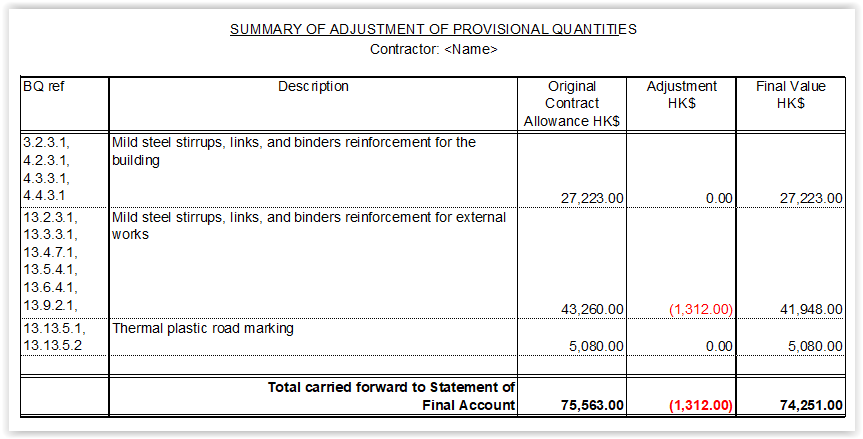

A Summary of Adjustment of Provisional Quantities may look like this: