Knowledge Base 知識庫

Knowledge Base 知識庫 KCTang-

This Knowledge Base is purely for the sharing of the knowledge of quantity surveying, and does not constitute as terms and conditions of our consultancy services. Our actual practice may vary to suit individual circumstances. This Knowledge Base shall not be used as evidence of practice and interpretations that we must adopt.

此知識庫純粹用作分享工料測量的知識,並不構成為敝公司顧問服務的條件及條款。敝公司的實際做法可能因應個別情況而有所變化。此知識庫不能作為我司必須採用某做法及釋義的依據。

-

This Knowledge Base was first published on Friday, 26th December, 2014 and was previously a WiKi site created on Thursday, 14th January, 2010.

此知識庫首先於2014年12月26日星期六發布,之前是一個於2010年1月14日星期四建立的 Wiki 網頁。

Quality Alerts 質量提示

Quality Alerts 質量提示 KCTangNote

- 17/3/2026 & 18/3/2026: Generally updated.

- 24/12/2024: "Estimates for maintenance and renovation" moved out to become its own page. "維修裝修估算"移往自己頁。"Measurement of quantities" moved to "Measurement and Billing" as "On-screen measurement". "計量"移往"計量和列單" 並改名為“螢幕計量”。

- 4/11/2015: Created. 建立。

Where is the satisfaction?

滿足感在那裡?

- Winning the trust of Clients, being consulted frequently.

客戶信任,時常諮詢。 - Problem solved.

解決到問題。 - Proper monitoring of prices, without unpleasant surprises to the Clients.

造價跟蹤管理得宜,不出客戶意料之外。 - Considered fair and reasonable by both the Employers and the Contractors.

發包方及承包方都覺得公平合理。

Invisible hand

無形的手

- Always be prepared to be audited by a third party.

隨時準備有第三者審計。 - Professional misconduct would cause damage to the Company not compensable by professional liability insurance.

專業失當就算有保險都不能補償對公司造成的破壞。

Treating the counter-parties

對待對手

- Fair.

公平。 - Reasonable.

合理。 - Non-corruptive.

廉潔。

Timely responses

(Section added, 18/3/2026)

- Take action within a reasonable time after the receipt of any request whether a deadline has been set or not.

- Give advice proactively if the incoming correspondence shows something contrary to the proper contractual interpretation or monetary amounts.

- Set reasonable time table well in advance for receipt of Tender Drawings and Specification for tender documentation.

- Comply with reasonable deadlines set by others.

- Do not encourage the habit of last minute requests with "sorry for the rush".

- Notify immediately if the deadlines set are unreasonable, and counter-propose a reasonable target dates.

- Ask for extension well before the deadline if the reasonable deadline becomes unachievable.

- Do not leave matter unattended for a long time without proper action.

Emails

(Section added, 18/3/2026)

- Watch out email size limits.

- Avoid using cloud storage links.

- See Use of emails - Quality Alerts updated on 18/3/2026.

PDF files

(Section added, 18/3/2026)

- Adopt the source file name as the file name of the generated PDF file, with the file extension changed to "pdf".

- Email back the source file after sending out the PDF file only.

- Assign a systematic file name for scanned PDF file showing the job number and title as the prefix.

Exchange of hardcopy of documents

(Section added, 18/3/2026)

- Despatch and collect documents according to the following customs:

- done by us for documents exchanged with the Clients and othe Consultants

- done by the contractors and sub-contractors for documents exchanged with them.

- Ask the other consutlants to send their Tender Drawings and Contract Drawings to the final destiny instead of through us to avoid unnecessary time and cost.

- Remind the party who has not collected a document from our office as requested on the day available for collection to collect.

- Pack the documents to be collected with waterproof sheets when raining.

- Send to that party for important document to avoid further delay if the document is still not collected.

- Insert a blank page as the last page before the back cover of hardcopy documents bound by clips or screws to protect the last page with information from wear and tear damage.

Folder and file naming

(Section added, 18/3/2026)

- Make the data or email folder names and filenames as concise as possible because too long folder + filename path may exceed the limit supported by the computers.

- Avoid to use spaces or full stops in folder names and filenames like "Payment valuation No. 1" because it is inconvenient for use via terminal command.

- Use camel case like "PaymentValuationNo1".

- Use "-" to mean different levels, such as "ContractA-PaymentValuationNo1".

- Use "_" before different versions or dates, such as "ContractA-PaymentValuationNo_1" or "ContractA-PaymentValuationNo_1_20260318a".

- Alternatively use brackets for dates, such as "ContractA-PaymentValuationNo_1(20260318a)".

- Use "+" for "&" because "&" may conflict with codes for Chinese characters.

- Prefix the file name with job number at least, possibly with short job title as well.

- Type in the file name in page header or page footer instead of using automatically updated file name field in case it is not wished that the file name should automatically be updated based on the actual file name used, e.g., in Tender Documents.

Correct terminology

(Section added, 18/3/2026)

- Use the terms used in the form of contract being used.

- Be aware that different forms of contract use different terms and expressions (SFBC, Govt GCC, NEC, etc).

- Use terms consistently within the same document.

- Use capitalised words consistently.

- Note the special styles of terms used in NEC contracts.

- Adopt the contract provisions exactly when those provisions are used when issuing certificates, comments on bonds and insurances, etc.

- Use correct grammar. See Common Errors in use of English.

- Use spellspeck offered by Word and Excel.

- Use AI tools to help check the grammar only.

- Do not necessarily adopt AI's suggested style or re-written text because it may not be consistent with the usual style used by the company.

- Be more specific as to the class and standard to be chosen when writing descriptions in the Bills of Quantities or Schedule of Rates.

- Refer to the specific Specification clause numbers in accordance with "as described in the Specification" when writing descriptions in the Bills of Quantities or Schedule of Rates.

- Avoid the use of broadbrush expressions like "as described in the Specification" and "as shown on the Drawings" without being specific as to the clause number or drawing number or reference number of the details or item number of the drawing notes, because these are superfluous with no additional use when other parts of the Tender Documents should have contained some provisions saying that the Bills of Quantities or Schedule of Rates must be read in conjunction with the Specification and Drawings.

Numerical accuracies

(Section added, 18/3/2026)

- Calculate the quantities based on the Tender Drawings or Instruction Drawings.

- Be cautious when using as-built drawings because they may show some work actually done but without entitlement to payment:

- done without Architect's instructions or subsequent confirmations of verbal instructions but accepted to remain

- done but not measurable separately according to the Standard Method of Measurement

- done but not measurable to the lengths as done according to the Standard Method of Measurement (e.g. cables and wirings).

- Observe the number of decimal places to be used in dimensions and quantities as specified by the Standard Method of Measurement, however:

- when the contractor's calculations do not strictly comply with the rules, whether the non-compliance should be strictly corrected should depend on the ultimate magnitude of the errors so caused

- if the total cost of the times to be spent by all concerned parties to correct these non-compliance is more than the amounts of the errors, it should not be worthwhile to make the corrections.

- Apply rounding off to the totals suitably because this can reduce the chances of consequential corrections when there are some minor errors in the build-up.

- Round up estimates:

- estimated quantities to whole numbers of 2 or at most 3 significant figures

- estimated rates to whole numbers of 2 or at most 3 significant figures

- estimated amounts to the nearest 10,000.

- Round off pro-rata or fair rates to the nearest 10 or a whole number of 3 significant figures, e.g.:

- if the contract rate is a round number of $1,200, a pro-rata may be arithmetically calculated as $1,345.67 but such apparent accuracy is inconsistent with the original contract rate. It should be rounded to $1,350

- for bigger numbers like $1,234,567, $1,250,000 should be acceptable.

- Round off gross valuation to the nearest $10,000 and retention to $1,000 such that the net valuation and net amount due are still rounded to $1,000.

- Round off the Final Contract Sum to the nearest $1,000.

- Obtain the Client's and the Contractor's consent to the rounding off rules.

- Ensure that the arithmetical formulae used are correct nothwithstanding the permission to round off.

- Build in an alternative formula to double check the accuracy of the totals.

- Double check all arithmetics by another person.

- Double check the BQ references of the contract rates used in the valuations.

- Carry out bulk-checking.

- State the name or initials of the person doing the primary calculations.

- Sign after all checking with initials or names of checking persons stated.

- Use red colour for first double-checking and green colour for corrections if the checking is done manually on paper.

Transfer checks

(Section added, 18/3/2026)

- Double check all transfer of figures from one place to another by another person.

- Update the Financial Report and draft Final Account whenever there is any update to the descriptions and amounts of the individual estimates or assessements.

- Update the next Payment Valuation accordingly.

Benchmarking

(Section added, 18/3/2026)

- Benchmark the total quantity ratios against similar projects when finishing the first calculations.

- Benchmark the total amount per suitable quantity against similar projects when finishing the first calculations.

- Review the net effect of the changes after updating and feel whether this is within the magnitude expected.

- Investigate why the net effect is beyond expectation.

Records of quality checks

(Section added, 18/3/2026)

- Record the names of the persons involved in various tasks (BQ production, financial reporting, payment valuations, final account assessments, etc.)

- Record in each document the names of the persons involved in that document.

- Ensure that all drawings used for measurement have been coloured or lined through to the full extent required to be measured.

- Do not colour or line through drawings before measurement.

- Ensure that the Preambles and the Specification clauses have been lined through to signify that they have been taken into account in the preparation of the Bills of Quantities or Schedule of Rates.

- Stamp quality check chop on the finished documents with proper initials and signatures by persons involved.

Calendar updating

(Section added, 18/3/2026)

- Register events or leaves on calendar prescribed by the Company.

- Adjust the entries in case of changes.

- Adjust the actual time spent immediately after the event.

- Record important deadlines for:

- fee submissions

- issue of tender documents

- return of tenders

- submission of periodical reports

- expiry of bonds and insurances

- renewal of own annual returns, business registration certificates, insurances, tenancy agreement, contracts for use of office equipment, etc.

Attending meetings

開會

- Be prepared.

要有準備。 - Watch out deportment.

注意儀態良好。 - Refrain from smoking.

不要抽煙。 - Present oneself appropriately.

洽當表現自已。 - Should not keep silence without contribution.

不要默不作聲毫無貢獻。 - Should not speak unnecessarily.

不作無謂發言。 - Say “To check and reply” if necessary cannot answer.

真的不會答時, 不怕答“容後補答”、“要查證再覆”。 -

Email back documents received or notes written at the meeting.

(Point added, 18/3/2026)

Price information

價格資訊

- Build-up a database.

建立資料庫。 - Collect directive circulars and prices published by Government and authorities.

收集政府、權力機構的指令性通知、價格。 - Collect market prices through other commercial sources (i.e. cost software vendors).

收集其他商業渠道的市場價格(例如造價軟件公司)。 - View newspapers, periodicals, internet.

檢閱報章、期刊、互聯網。 - Collate internal information.

整理自身的資料。 - Analyse content ratios and unit costs of past projects.

分析過往工程含量及單位造價。 - Obtain through tendering.

通過招投標取得。

Cash flow table

資金流量表

- Use horizontal table with a chart.

盡量使用橫式有圖表那個款。 - Include complete remarks.

要加齊註釋。

Standard documents

標準文件

- Use standard documents/templates to prepare fee proposals, tender documents, tender reports and other documents, but may refer to other projects for useful changes.

要用標準文件編寫顧問費報價、招標文件、投標分析報告及其他文件,但可參考其他工程有用的改動。 - Do not adapt from other projects, unless really appropriate, but should check the standard documents for any updates.

不要直接用其他工程的改, 除非真的合適,但仍要核對標準文件有無最新的改動。

Lead in water problem

鉛水問題

- Check tender documents for expressions using lead, and check with the designers whether this is appropriate.

檢查招標文件有無用鉛的字句,及與設計單位了解是否適合。

Insurance provisions in tender documents

招標文件保險條款

- Ensure that the name list of the joint-insured as specified in the Contractors’ All Risks and Third Party Liability insurance provisions is comprehensive; apart from the Employer, the Contractor and sub-contractors of all tiers, note whether the list should include:

確保規定工程一切險及第三者責任險的條款的聯名被保險人的名單齊全;除發包方丶承包方及各層分包方外,還要注意是否要加入:- the Building Manager (being a manager of the relevant properties, he may be held liable)

物業管理人(因他為相關物業的管理人,可能被追討責任) - other contractors employed by the Employer (because their works will be carried out currently with the Works, and the liability for accident may not be clearly separable)

發包方聘用的其他承包商(因其工程與本工程同時執行,意外責任未必能分得清) - consultants (because they are not directly performing the Works, and the insurances can only cover risks caused by the performance of the Works, therefore, it is doubtful whether they should be included as one of the joint-insured).

顧問(因他們不是直接執行工程者,而保險只保障執行工程所造成的風險,因此,把他們作為聯名被保險人之一的效用存疑)。

- the Building Manager (being a manager of the relevant properties, he may be held liable)

- Adjust the old term “separate specialist contractor” to match the term used in the new Standard Forms of Contract.

調整“separate specialist contractor”這舊有叫法以符合新標準合同的叫法。 - State the values of their works for inclusion as part of the sum insured to avoid inadequate insurance cover.

列出他們的工程金額,作為保額的一部分以免保額不足。 - State expressly work outside boundaries to avoid lack of insurance cover.

特別列出工地外的工程以免保險範圍甩漏。 - Include in the amount of removal of debris the costs of demolition of building, hoardings (if not included in the present contract), scaffolding for demolition, etc; review whether the $1M stated in the standard documents are adequate and adjust as appropriate.

計算保險的殘礫清理保額時要包括拆樓、圍街板(假設本合同價未包括圍街板)及拆樓用的棚架;檢討標準文件寫的100萬元是否足夠及作適當的修改。 - State the values of the previous works such as foundations and hoardings for inclusion as part of the sum insured under the material damage section to ensure full cover; alternatively, if the risk of total loss is low, insure as the principal’s properties under the third party liability section, but the limit of indemnity will be lower.

列出之前的工程,例如基礎、圍街板等的價值,加入物質損壞保險的保險額內以取得全額保;或者,如全毀的風險低,可以作為工程委託方的財産形式在第三者保險部份受保,但賠償額較低。 - Require the CAR insurance to include an escalation clause if the contract period is more than 1 year to allow for inflationary increase to the amounts insured based on the original contract sum. This escalation clause may also help towards increased contract sum due to variations exceeding the contingency sum.

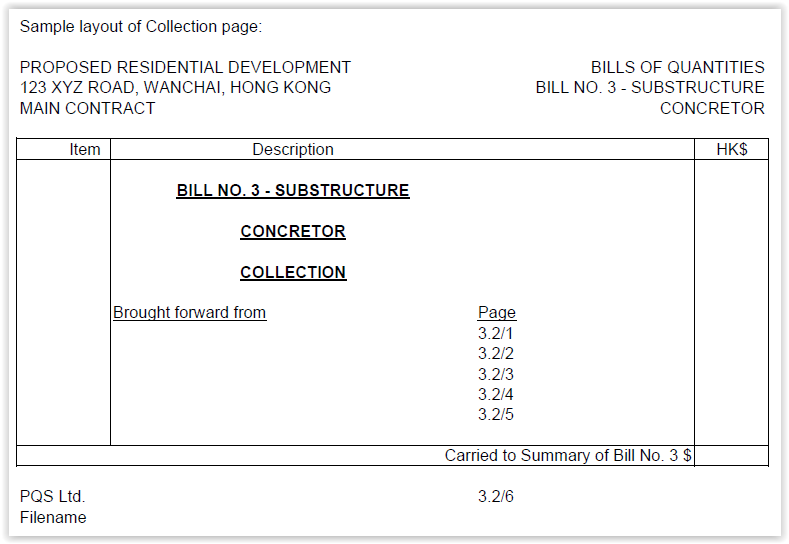

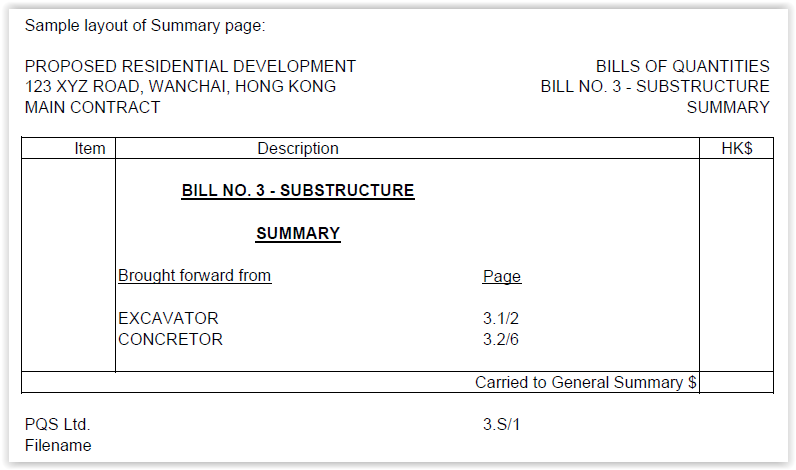

Preparing Bills of Quantities or Schedule of Rates

編寫工程量清單或單價表

- Read the Standard Method of Measurement, whether you are experienced or not; do not just listen to other people.

任何時間都要睇工程量計算規則,無論生手定熟手,不要光聽人講。 - Note concrete mix, beam depth stages, height stages, edges, shoulders, straight / sloping / curved, etc.

計混凝土工程時要注意混凝土的標號、樑深的層級、高度的層級、邊沿、接肩、直斜彎,等等! - Do not blindly follow past Bills of Quantities or Schedule of Rates because they may have simplified the measurement which may not be applicable to every project, and may in fact be wrong.

不能盲目照跟舊有的工程量清單或單價表因為它們可能把計法簡化了,但此不是單單工程都合用,而其實可能根本就錯了。

Preliminaries Bills

開辦營運費清單

- Draw horizontal lines to separate items in Preliminaries Bills containing clause headings only to enable entry of prices in alignment with the item descriptions

用橫線把只列條款標題的開辦營運費清單內的項目間開以便填寫價格時對齊項目說明。

Rates of liquidated damages

(Section added, 18/3/2026)

- Ask the Clients for the rates of liquidated damages to be used (though very often they ask us to suggest) because only the Clients can really know the loss and expense which may be suffered by them due to delayed completion of the Works.

- In case of sectional completion, the rates applicable to the various sections should commensurate with the values which may be generated from the sections completed. If two very different sections have the same rates of liquidated damages, it can be challenged that one of the rates is a penalty not enforceable.

Specification

(Section added, 17/3/2026)

- Ask the relevant design consultants to prepare their Technical Specification.

- Reflect the requirements of the Technical Specification in the Bills of Quantities or Schedules of Rates.

- Help reduce errors, inconsistencies and ambiguities in the Technical Specification.

- Do not correct their Technical Specification on their behalf.

- See Specification - Quality Alterts updated on 17/3/2026.

Tender Documents

(Section added, 17/3/2026)

- Keep a printed copy of the Tender Booklets and Tender Drawings as a control copy.

- Do not rely on reading the soft copies.

- Update the pages with those issued under any tender addendum.

Tender invitations

(Section added, 17/3/2026)

- Plan well the time schedule for issuing Tender Documents and return of tenders when the tendering period is spanning over long holidays especially the Chinese New Year holidays when factories, suppliers and sub-contractors may close down for holidays.

Documentary exchange with tenderers

與投標者的來往文件

- Keep the hardcopies and softcopies of documents, correspondence, faxes and emails exchanged during tendering under a separate folder for each tenderer to enable easy tracking and compilation of contract documents.

把招投標標的 所有來往文件、信件、傳真及電郵的打印或電子件按每一投標者分開歸檔,以便追蹤及製作合同文件。

Tender clarification queries

詢標問卷

- Clarify in the tender clarification queries only those incorrectly priced high or low rates, not comparatively high or low rates

在詢標問卷應只問錯誤地高或低的單價,而不是相對高或低的單價。

Deeming unpriced items as included

(Section added, 18/3/2026)

- Include in the Tender Documents a clause stated that any items listed in the Bills of Quantities but not specifically priced by the tenderers shall be deemed to have been priced elsewhere in the Tender Sum.

- Include in the Tender Documents a clause stated that any work shown on the Tender Drawings or described in the Tender Specification but not specifically priced by the tenderers shall be deemed to have been priced elsewhere in the Tender Sum.

- It is common that many items in the preliminaries would not need a specific price against them.

- Do not need to issue tender clarification queries to the tenderers to confirm the above because the implications have already been stated in the Tender Documents.

- Do not deem those unpriced items as priced at "$0" because this would become a contract rate to be used for pricing variations. If there is an omission, the amount to be omitted will still be zero.

- On the other hand, if an item deemed included in the Tender Sum / Contract Sum is omitted, it should still be possible to omit the relevant costs saved. Of course, this may equally apply to variation additions. A distinction may be based on whether the deemed included items are ancillary items to other specifically priced principal items. If they are, then they themselves will not be omitted or added when the quantities of the principal items are not changed. If they are not ancillary items but are standalone items, it should be fair to make reasonable cost adjustments if their quantities are increased or reduced based on the relevant costs.

Tender Reports

(Section added, 18/3/2026)

- State the site address in the tender report.

- State also the site area and total gross floor area in the tender report to facilitate cost per area calculation.

- Describe briefly the Main Contract scope of works in the Sub-Contract tender reports.

- State the estimated budget in the Main Contract tender report or the PC Sum the Nominated Sub-Contract tender report.

- Extend the tender validity period if the contract cannot be awarded before the expiry date and the project is still alive.

Contract Documents

(Section added, 18/3/2026)

- Collate the Contract Documents for signing as soon as possible after the award of the contract, even though a binding contract has come into existence upon the issue of the letter of acceptance not refused by the Contractor.

- Co-ordinate with the other consultants to make sufficient copies of Contract Drawings.

- Remind them to use the set issued for tendering.

Extension of time claims

(Section added, 18/3/2026)

- Advise only on the contractual validity of an extension of time claim with reference to the extension of time clauses relied upon.

- Leave the ascertainment of the extent of the delay and extension of time to the Architect. It is his privilege and duty to do so.

Financial reports

最終造價估算報告

- Estimated Amount = Reasonably estimated maximum amount for budgetary purposes

估計價 = 合理估計的最大金額,供投資預算用。 - First Claimed Amount = Amount initially claimed or the biggest amount claimed by the Contractor

原報價 = 承包商第一次或最大的一次的報價。 - Latest Claimed Amount = Latest revised amount claimed by the Contractor, or the current amount after negotiated reduction

最新報價 = 承包商最新的修訂報價,或通過談判應已減低了的金額。 - Assessed Amount = Amount accurately or roughly assessed to be comfortably payable finally, in other words, the minimum final amount payable

審核價 = 經準確或大約計算得的可安心作為最終應付的總額,亦即等如最低的最終應付總額。 - When Assessed Amount = Claimed Amount, Estimated Amount should also be = Assessed Amount

當審核價 = 報價時,估計價亦應 = 審核價。 - In the final stage of final account, the Estimated Amount should be smaller than the Claimed Amount

到結算後期,估計價應低於報價。 -

When an instruction is for the expenditure of a provisional sum, the amount should be entered as an expenditure of the provisional sum. The unexpended amount of the provisional sum should be retained for future use by adding an item for "allowance for potential expenditure".

(Point added, 18/3/2026)

Approximately

大約

- Write “approximately X Nos.” instead of “approximate X Nos.”

寫成“approximately X Nos.” 而不是 “approximate X Nos.”

Replace by or with

更換

- “replace by” or ”with” may be distinguished by this example: in “replace A by B with C”, A is the replaced, B is the one who takes action, and C is the substitution

“replace by”定”with” 可以此例子分辨:”replace A by B with C” 中A是被更換者、B 是行動者、C是代替者。

Final account item descriptions

結算項目說明

- Note that if the words "revise", "change", "replace" and similar are used in the final account item descriptions, cost omission and addition are both expected

注意當”修改”、”改變”、”更換”等類似用詞在結算項目說明使用時,意味應同時有減帳及加帳。 - Make sure that the final account item descriptions are consistent with the cost effects

確保結算項目說明是與費用影響匹配。

Personnel Organisation 人員編制

Personnel Organisation 人員編制 KCTangNote

20 Dec 2014: Moved form wiki.

Personnel organisation to consider

人員編制要考慮

- How many people

要多少人 - Types and number of professional personnel

專業人員的類別及人數 - Types and number of supporting personnel

輔助人員的類別及人數 - Continuing learning

持續學習

Kind of persons to employ

請什麼類形的人

- Enduring

克苦 - Hard working

實幹 - Attentive to details

細心 - Highly analytical

分析力強 - Eager to learn

肯學習 - Able to use computer

會用電腦 - Able to use common office software

會用常用的辦公室軟件 - Literate in Chinese and English

具中英語文能力

Administrative Management 行政管理

Administrative Management 行政管理 KCTang Note 注

- 19/1/2023: Updated to reflect the established practice.

更新以反映既定慣例。 - 30/7/2021: "Use of recycled paper" added.

添加了“回收紙的使用”。 - 13/7/2021: "Sending back source files" added.

添加了“發回源文件”。 - 7/7/2021: "Use of emails" expanded. "Filing of letters and emails" added.

擴展了“電郵的使用”。 添加了“信件和電郵的歸檔”。 - 7/4/2019: "Issuing Tender Documents just before holidays" added.

添加了“臨假期前出標”。

Joining the Company 加入公司

- Company:

公司:- Add new member's name to company address book (using Google Contacts).

將新成員的姓名添加到公司地址簿(使用 Google 通訊錄)。 - Create a Google calendar for the new member.

為新成員創建一個 Google 日曆。 - Assign a name for the calendar in the format of "AB.Ccc" where AB are the initials and Ccc is the family name.

以“AB.Ccc”格式為日曆分配名稱,其中 AB 是首字母,Ccc 是姓氏。 - Give the Google account name and password to the new member.

將 Google 帳戶名和密碼提供給新成員。

- Add new member's name to company address book (using Google Contacts).

- New member:

新成員:- Sign in the Google account to access the calendar and contacts.

登錄 Google 帳戶以訪問日曆和聯繫人。 - Fill in own full name in English and Chinese (if applicable), office phone number, private email address and private phone number.

填寫自己的中英文全名(如適用)、辦公室電話號碼、私人電郵地址和私人電話號碼。 - Record own daily office appointments and leaves on the calendar.

在日曆上記錄自己每天的辦公室約會和休假。 - Update the times after finishing the appointments.

完成約會後更新時間。 - Change the name of the computer and user name on the computer assigned for use to reflect own name.

在指定使用的電腦上更改電腦名稱和用戶名以反映自己的名稱。

- Sign in the Google account to access the calendar and contacts.

(added 添加, 19/1/2023)

Office Hours 辦公時間

- Office:

辦公室:- Normal office hours from 8:45 am to 5:45 pm from Monday to Friday except general holidays.

正常辦公時間為周一至周五上午 8:45 至下午 5:45,公眾假期除外。 - Lunch hour from 1:00 pm to 2:00 pm.

午餐時間 1:00 pm 到 2:00 pm。 - Normal office hours must be fulfilled before counting for overtime.

在計算加班時間之前,必須完成正常的辦公時間。

- Normal office hours from 8:45 am to 5:45 pm from Monday to Friday except general holidays.

- Staff members:

職員:- Clerks must be punctual for the normal office hours.

文員必須準時上班。 - Some slight late arrivals of other staff members is tolerable but up to 9:30 am only.

其他職員員的一些輕微遲到是可以容忍的,但僅限於上午 9:30前。 - Any late arrival beyond that should be compensated by an equal amount of working time with no pay after fulfilling the normal office hours.

超過此時間的任何遲到都應在完成正常辦公時間後以等量的無薪工作時間作為補償。 - Sign in and out whenever they come and go.

每當出入時都要簽到和簽出。 - Fill in the timesheets everyday before leaving the office or just after coming back on the next day. (Timesheets will be subject to sample checks for salary payment purposes. If more than the actual time is recorded, the recorded time will be discounted based on the percentage error for salary payment purposes.)

每天在離開辦公室之前或第二天剛回來時填寫考勤表。(計算薪酬時,會抽樣檢查考勤。如記錄超過實際的時間,計算薪酬的時間將按百分比誤差打折扣。) - Get the director-in-charge's consent before taking casual / annual leave.

休事假/年假前須徵得主管董事的同意。 - Notify all colleagues through WhatsApp before taking sick / casual / annual leave (the day before in case of pre-planned leave).

在病假/臨時假/年假之前用 WhatsApp 通知所有同事(如果是預先計劃的假期,請提前一天)。 - Submit doctor's certificate for sick leave afterward.

之後提交病假醫生證明。

- Clerks must be punctual for the normal office hours.

(Added 添加, 19/1/2023)

Issuing Tender Documents just before holidays 臨假期前出標

- If issuing Tender Documents on Friday, remind the tenderers that our office is closed on Saturday and not available for collection of documents.

若星期五出標,提醒投標者敝公司星期六不辦公、不要到取文件。 - If issuing Tender Documents just before the Chinese New Year Holidays, ensure that the tendering period can accommodate the different lengths of holidays of the tenderers and their suppliers and factories. Factories usually close for longer time than the public holidays.

若臨農曆年假前出標,確保投標期可以包容投標者及他們的供應商及工廠的不同的假期長度。工廠通常放假較公眾假期長。

(Added 添加, 7/4/2019)

Office appliances 辦公用具

- Paper

紙張- Use recycled paper as much as possible.

盡可能使用再生紙。 - Print on single side of new paper.

在新紙上單面打印。 - Reserve the other side for recycled use.

保留另一頁以供回收使用。 - Avoid printing on both sides because it will increase the workload when sorting out single and double sided printed paper in the future for scanning or disposal.

避免雙面打印,因為這會增加日後整理單雙面打印的紙張進行掃描或處理時的工作量。 - Print on both sides for thick documents only.

僅厚文檔用雙面打印。

- Use recycled paper as much as possible.

- 4-in-1 Printer, photocopier, scanner and fax machine

4 合 1 打印機、複印機、掃描儀和傳真機- Rotate the use of recycled paper on different machines to reduce the wearing on any particular one.

在不同的機器上輪換使用再生紙,以減少任何個別機器的磨損。 - Rotate once every month.

- 每月輪換一次。

- Rotate the use of recycled paper on different machines to reduce the wearing on any particular one.

- Binding machine

釘裝機 - Telephone

電話 - Broadband connection

寬頻接線 - Internet service

互聯網服務 - Intranet

內聯網 - Computer

電腦- Close software when leaving the desk for long.

長時間離開辦公桌時關閉軟件。 - Switch off the computer after leaving the office (except when remote desktop is required for use).

離開辦公室後關閉電腦(需要使用遠程桌面時除外)。

- Close software when leaving the desk for long.

- Client software

客戶端軟件- Office automation - Windows 10 and 11, Office 360.

辦公自動化 - Windows 10 和 11、Office 360。 - Pdf and compression - Acrobat, Wondershare, WinRar.

Pdf 和壓縮 - Acrobat、Wondershare、WinRar。 - CAD and BIM - Autocad, Intellicad, Revit.

繪圖及立體資訊模擬 - Autocad、Intellicad、Revit。

- Office automation - Windows 10 and 11, Office 360.

- Server software - Ubuntu

伺服器軟件 - Ubuntu- File server - Samba.

檔案伺服器 - Samba。 - Email server - Postfix and Dovecot.

電郵伺服器 - Postfix 和 Dovecot。 - Web server - Drupal.

網頁伺服器 - Drupal。

- File server - Samba.

(Updated 更新, 19/1/2023)

Passwords 密碼

- Unless authorised, do not watch, memorize or use passwords used by the Company to assess internal or external websites.

未獲授權不應觀看、記下及使用公司使用的內外網站的密碼。 - Do not disclose passwords used by the Company to outside persons.

不得對外人披露公司使用的密碼。

Fax machine setting 傳真機的設定

- Set time clock.

設定時鐘。 - Set sender’s identity.

設定發送者的識別。

Printer driver 影印機的驅動程式

- Do not install those provided by Windows.。

不要安裝Windows 提供的。 - Install those provided by the printer companies.

安裝打印機公司提供的。 - Copy the file saved in the “Installation Sources” folder in the server to the local computer, install, set to use A4, black and white, single sided and recycled paper, and delete the file after successful installation

把存儲在伺服器”Installation Sources”檔案夾內的安裝檔抄到自己電腦,安裝,設定用A4、黑白、單面、再用紙,裝後刪除安裝檔。

Protocol when answering phone calls 接聽電話的禮儀

- Answer first with company name or own name.

先報上公司名稱或自已名稱。 - Pick up phone calls for other colleagues when they are not at their desk.

當其他同事不在辦公桌前時,為他們接聽電話。 - Ask for the name, contact number, company and project name of the calling person and record on a paper.

詢問來電人的姓名、聯繫電話、公司和項目名稱,並記錄在紙上。 - Take photo of the paper note and send immediately by WhatsApp to the colleagues intended to be called for follow-up.

拍照紙上筆記,並立即通過 WhatsApp 發送給被找的同事跟進。

(Updated 更新, 19/1/2023)

Use of recycled paper 回收紙的使用

- Recycle paper which has been printed on one page only.

回收再用僅打印在一頁的紙。 - Only recycle paper which is in good conditions and does not have stamped marks on the printed page visible on the blank page.

僅回收狀況良好且在空白頁上不會見到打印頁上的印記的紙張。 - Use recycled paper to print emails and drafts not intended for sending out as hardcopies.

使用回收紙打印不打算作為硬拷貝發送的電子郵件和草稿。 - Do not send out recycled paper to outside parties because it may contain confidential information.

不要將回收紙發送給外方,因為它可能包含機密信息。 - Put recycled paper in the standby storage boxes and printer trays following the facing directions indicated at the standby storage boxes or printers.

按照備用儲物箱或打印機上指示的朝向,將回收紙放入備用儲物箱和打印機托盤中。 - Inspect the recycled papers to be free of staples and in the correct directions before putting them in the printer trays.

在將回收紙放入打印機紙盒之前,檢查回收紙是否沒有釘書釘並且方向正確。 - Put the recycled paper in the printer trays in such a way that the previously printed page will be on the back and upside down a後fter re-printing.

將回收紙放入打印機托盤中,使之前打印的頁面在再打印後在背面倒置。 - Draw a diagonal line after re-printing on the last back page of such recycled paper.

在再打印後在最後一頁畫一條對角線。 - Draw a diagonal line after re-printing on each of the previously printed pages not turned upside down .

在再打印後在沒有倒置的舊打印頁的每頁畫一條對角線。 - Note that recycled pages which do not have the previously printed pages turned upside down will cause confusion when reading and when the document is to be scanned in the future.

注意,沒有將舊打印的頁面倒置的回收紙會在閱讀時和將來掃描文檔時造成混亂。

(Added 添加, 30/7/2021)

(Updated 更新, 19/1/2023)

Use of emails 電郵的使用

(Expanded 擴展, 7/7/2021)

(Updated 更新, 19/1/2023)

Generally

一般

- Follow the template for folder structure under the email Data folder to create new folder structure for new jobs.

參照Data電郵夾下的電郵夾結構模板” template for folder structure” 的概念把所有工程的電郵夾分類及統一名稱。 - Do not print emails except when printed copies are required for use (particularly when drawings are to be printed for taking-off and colouring for evidence of taking-off).

不要打印電郵,除非需要使用打印副本(特別是當需要打印圖紙以進行計量和著色以作為計量證據時)。 - Delete spam emails on sight, to reduce everybody’s abortive time to read (permanent clearance from the Deleted Items folder will be done by the Administrator).

一見垃圾電郵就立刻刪除,以免人人都要花時間看(從刪除郵件夾永久刪除由管理員做)。 - Ignore all emails received from time to time calling for security verification regarding iTune, Apple ID, Microsoft, PayPal, HSBC, etc. since they are mostly malicious emails.

千祈不要理會不時收到的關於iTune、 Apple ID、Microsoft、PayPal、HSBC 等等要人重新輸入認證的電郵,黑郵居多。 - Do not open or save attachments received from unknown persons, and do not click open links.

不要打開或儲存來自不認識的人的附件,亦不要打開連結。

Sending emails

發送電子郵件

- bcc all outgoing emails back to our office.

發出所有電郵時,密件抄送回自己公司。 - Check that the bcc copies are received by our office to prove that the outgoing server is working.

檢查自己公司是否收到密件抄送副本,以證明發送伺服器正常工作。 - Check that there are no delivery failure message (should appear within 5 minutes) to prove that the delivery is successful.

檢查沒有發送失敗消息(應在 5 分鐘內出現)以證明發送成功。 - Handle any delivery failure immediately by contacting the intended recipient for the proper address, and re-send with a remark "Re-sent due to delivery failure", cc all others on the original email to make them know.

立即處理任何送達失敗,聯繫預期收件人以獲取正確地址,重新發送,註明“因送達失敗而重新發送”,並抄送原始電郵中的所有其他收件人以知會他們。 - For urgent email failed to be delivered after retry or failure to contact the intended recipient, fax the email copy to his/her company with a remark "Faxed due to email delivery failure" and the date. Email the front page back to the office.

緊急電郵在重試後仍未能送達或未能聯繫到預期的收件人,將電郵副本傳真給他/她的公司,並註明“因電郵送達失敗而傳真”和日期。 將首頁通過電郵發回自己公司。 - Email source files (Word, Excel, etc.) back to our office after sending out pdf files. Mark at the beginning "Source files attached".發送 pdf 文件後,將源文件(Word、Excel 等),電郵發送回自己公司。 在開頭標記“附加的源文件”。

Correspondence not by emails

非電郵的來往文件

- All outgoing and incoming documents not sent by email should be emailed back to our office for the record on the same day.

所有非通過電郵發送的來往文件應在同一天通過電郵發送回自己公司以資記錄。

Printing frequency (no longer adopted)

打印頻率(不再採用)

- Print all emails once every half-an-hour as far as possible.

盡可能每半小時打印一次所有電郵。 - Print before lunch break all emails received before 12 am.

午休前打印所有在上午 12 點之前收到的電郵。 - Print before close of a day's work all emails received before 5 pm.

在一天的工作結束前打印下午 5 點之前收到的所有電郵。 - Print upon starting a day's work all emails received before that.

在開始一天的工作時打印之前收到的所有電郵。

Persons responsible for filing emails

電郵歸檔負責人

- Be responsible for filing the softcopies of emails of their own projects.

- Assign more junior or newly joined staff members to file softcopies of emails for a team of staff members.

- Define filters.

- Clerical staff (if available):

- Assign a person as the final guard to remind all others to print their emails by the 12 am and 5 pm deadlines, and print all remaining emails not falling within the scope of the any particular team.

- The above principle still applies if a clerk is employed to do the printing.

Printing

- Print the newly received pages of the emails only, i.e., excluding linked pages of past emails which have been received before.

- Print on one-sided recycled paper. (One-sided printout will be easier for reading and future scanning for archiving.)

- Print on double-sided paper only when required by the surveyor responsible.

- Print the one with track-changes if both Word or Excel and pdf files are received.

Not to print

- Delete spam emails.

- Delete promotional emails not relevant to our industry, profession or business.

- Do not delete nor print promotional emails relevant to our industry, profession or business. File them under their relevant folders, if available, otherwise under "Sales Promotion".

- Permanent deletion from the Trash folders should only be made by the director.

- Do not print documents which are too thick, say more than 30 pages. Ask the surveyor responsible to see whether the thick documents should be printed.

Emailed copies of faxes

- Treat emailed copies of faxes similarly.

- Convert emailed copies of faxes to proper emails by forwarding each email with attached fax back to the office but stating a proper subject title and inserting an image of the first page in the email beforehand.

Documents sent through links

- Do not download from links sent by unknown senders for unknown purposes. Check with the senders if in doubt.

- Download ALL documents received through genuine links and and email them back to our office for the record.

- Email ALL documents sent out through links back to our office for the record.

- Split them into several emails if the file size is too large.

Emails attached to emails

- Save emails attached to an email received on to the computer desktop and move them back to the email folder. They will appear at the positions of their original email dates. This would enable reading the story in a chronological order, and easy tracing later.

- Print such emails like other emails.

Handling of printed emails

- When there are more than one attachment, identify whether they belong to one submission or several submissions each bearing its own serial number or date (e.g., letters, site memos, proposed variations, instructions, variation quotations, payments, minutes, regular reports, etc.).

- Separate between different submissions by staples or clips.

- Arrange different submissions according to the dates stated on them (not the dates received).

- Within the same submission, arrange the attachments in logical sequence, usually covering letter or site memo at the front and drawings at the back. Descriptive documents are usually in the middle. Summaries may be put before or after the details depending on the authors. Follow the specific contents page or the list of items stated in the email. Do not follow the order of the attachments to the email because they have no logical sequence.

- Fold thin A3 attachment (say, not exceeding 5 pages) forward from right to left along the centre line into A4 size, and then fold the top flap from left to right along the centre line into half A4 size.

- Fold thick A3 attachment backward from right to left keeping the edge clear from the left punch holes.

- Stamp the date received on the top right hand corner of each separate submission received (but no need for different parts of the same submission which are not supposed to be taken out for use separately).

- Stamp the date received on the top right hand corner on each programme and on the bottom right hand corner on each drawing because they may be filed or taken out for use separately.

- Mark near the date chop the relevant instruction numbers.

- Stamp neatly and clearly at a blank space.

- Do not stamp on submissions emailed by our office unless they are returned with emails received.

- Write on the emails simple reference numbers and dates of those separate submissions which are filed not immediately after the relevant emails to enable future tracing.

- Initial neatly on the bottom left corners of the emails after arranging the emails and attachments.

- File the emails directly in the appropriate email sub-folders of the relevant projects.

- If the emails are printed by somebody other than the relevant team members, file the emails under the "00Printed" email folder for subsequent filing by the relevant team members.

- Distribute the printed emails once every half-an-hour to the relevant project team members for reading.

- Circulate within the relevant team starting from the director to the assistant. If any person is absent, pass on to the next one present.

- Read and initial on the top right hand corners of the emails and the first pages of separate submissions.

- Take immediate actions as required by the emails.

- File the emails in the relevant hardcopy folder after all team members have read and initialled and when no further immediate action is required.

- File different submissions according to their dates even though those dates may be sometime in the past so that they can tell the complete story when the files are read sequentially sometime later. The date received stamp can help to trace that emails sending them though the submission and the email may be filed separately.

Filing of letters and emails 信件和電郵的歸檔

(Section added, 7/7/2021)

- Create a separate folder section for each preliminary cost estimate, proposed instruction, confirmation of verbal instruction, formal instruction, other item to appear in the final account (e.g., group of provisional quantities, provisional sum), financial report, payment valuation, etc.

- Name the email folders or label the hardcopy folder flysheets by their serial numbers.

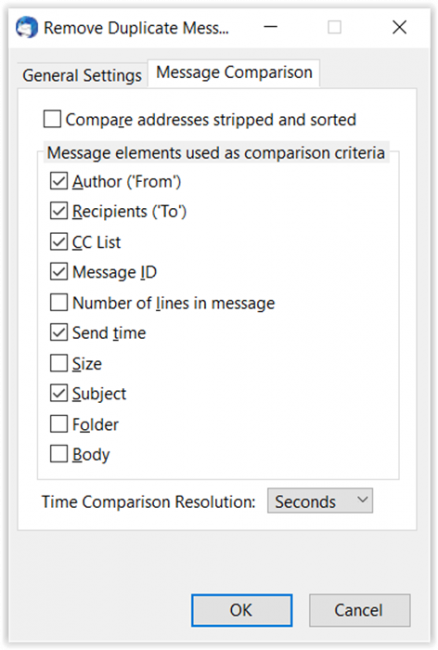

- If an email covers more than one folder section, email it back to the office with a note added to the subject so as to distinguish. Do not just make copies because identical copies will be deleted if a "remove duplicate" check is done.

- File requests for estimates and estimates under the proposed instruction folders. Move them to the formal instruction folders after the issuance of the formal instructions.

- Move confirmations of verbal instructions to the formal instruction folders after the issuance of the formal instructions.

- Change the folder or label names to reflect or track the move.

- File quotations and assessment related to a formal instruction under the same folder section, i.e., all matters related from cost estimate until agreement are to be filed together to tell the complete story.

- Spilt into more folders if an instruction covers more than one variation or final account item.

- Update the financial report descriptions and amounts to match whenever a new or revised quotation or assessment is received or issued.

- File communications with each tenderer separately. This is important for tracking the development, preparing the letter of award/intent, and contract binding.

- In principle, all incoming and outgoing documents in the email folders and hard copy folders should mirror each other, except for working documents not sent out.

- Bind tender documents as a book, not to be filed.

Archiving old hardcopy documents

(Section added, 30/3/2026)

- Do the following when archiving old hardcopy documents after completion of the relevant job as directed by the Director-in-charge.

- Try to do each process in one go for all folders and all jobs to be done, instead of doing many processes for one folder at a time.

- Photocopy the spine of the folder showing the job number, job title and subject, to serve as the cover sheet.

- Write similar information on a paper, if there is no such proper folder.

- Take away all the printed emails except those marked with working details.

- Take away those flysheets which do not have hardcopy documents left for them.

- Recycle or dispose of the pages taken away, if consented by the Director-in-charge.

- Remove all the staples, clips and strings from the paper to be recycled, and put the printed pages in the same orientation before putting into the recycling box for photocopier.

- Put the cover sheet, remaining pages including flysheets of each folder in a plastic folder until all the folders have been cleared.

- Scan all the pages in each folder as one PDF.

- Remove all the staples, clips and strings before scanning.

- Use double-sided scanning if the documents are predominantly double-sided.

- Use single-sided scanning if the documents are predominantly single-sided, but photocopy the back side of double-sided sheets and insert them back into the documents to facilitate single-sided scanning in one go.

- Use black and white mode for text documents.

- Use colour mode for documents with photo images. (Colour: greyscale : black and white size ratio : 1:12.4: 13.3. Colour : greyscale = 1 : 1.07.)

- Double check that there are no missing pages and the scanned output is legible.

- Use PDF editing software to reduce the file size if it can be reduced without significant change to the legibility.

- Email the PDF back, and file in the relevant email job folder.

- State the job number, job title and subject in the email subject. Do not need to state the date of the file in the email subject. Do not need to insert an image of the first page of the PDF in the email.

- State the date of the file in brackets at the beginning of the email subject, and insert an image of the first page of the PDF in the email, in case of emailing back a file instead of a PDF of many files.

- Write the initials of the email sending in the email.

- Recycle or dispose of the scanned documents, if consented by the Director-in-charge.

Use of WhatsApp 短信的使用

- Read Company chat group regularly.

- Reply immediately upon receipt of messages relating to self or all people, whether within or outside office hours.

在公司群組收到關於自已或關於全部人的短訊要即覆 - Report after completion of the task.

在事件完成後要報告 - Delete messages after completion of the task.

- Learn from others' messages to avoid committing the same mistakes and to adopt good practice.

- Delete non-relevant messages not worth keeping.

Revit

- Use the License Transfer Utility provided by Revit to transfer Standalone License from one computer to another computer without infringing the license

使用Revit提供的許可證轉移工貝(License Transfer Utility)把單機許可證從一部電腦, 轉移到另一部機而不違反許可證 - Use Revit 2015 because some outside companies still use Revit 2013 or 2014 and models of new version cannot be converted back to older versions

使用Revit 2015版,此乃因為外面有些公司仍只用Revit 2013或2014版,但新版本的模型不能改回舊 - Use Revit 2015 for trial

2016版屬試用

Documentary system 文書機制

- Use standard documents and templates

使用標準檔、範本 - Implement file management

執行檔案管理 - State file names, reference numbers, project names, contract names, subjects

註明檔案名稱、編號、項目名稱、合同名稱、主旨 - State date of receipt or dispatch, and affix acknowledgement chop

註明收發的日期及蓋簽收章 - Carry out internal check

執行內部審核 - Double-check after printing

列印後要覆核 - Double-check after calculating

計算後要覆核 - Double-check after transferring figures

搬移數字要覆核 - Check quantities and rates

覆核數量、單價

File compression 檔案壓縮

- Set Winrar to use zip format to enable users who do not have Winrar to open (Windows file explorer can open zipped files)

把Winrar 檔的格式設定為zip方便沒有Winrar的人打開(Windows file explorer可打開zipped 檔

Generate pdf file from Word file 轉換 Word 檔成 pdf 檔

- 按以下優先次序以減少檔案大小:

- Print CutePDF (如有)

- Print - Save as Adobe PDF (如有)

- Print - Adobe PDF (如有)

- xport

- Save as

Travelling expense 交通費

- State the destination on all taxi fare receipts for the record

在所有的士單據上列明目的地,以作記錄

Use of toilets 衛生間的使用

- Use the toilet roll plastic wrapper after unwrapping as the base cushion to the toilet roll to avoid wetness and reduce dirt

把廁紙膠套在剝除後用作廁紙的座墊,以便防濕及減髒 - Place a new roll as reserve when the toilet roll is about to be used up

廁紙接近用完,主動取放一卷作後備

Use of Emails 電郵的使用

Use of Emails 電郵的使用 KCTang Note 注

- 18/3/2026: Split from "Administrative Management". Quality Alerts added.

- 7/7/2021: Expanded 擴展.

- 19/1/2023: (Updated 更新

Generally 一般

- Follow the template for folder structure under the email Data folder to create new folder structure for new jobs.

參照Data電郵夾下的電郵夾結構模板” template for folder structure” 的概念把所有工程的電郵夾分類及統一名稱。 - Do not print emails except when printed copies are required for use (particularly when drawings are to be printed for taking-off and colouring for evidence of taking-off).

不要打印電郵,除非需要使用打印副本(特別是當需要打印圖紙以進行計量和著色以作為計量證據時)。 - Delete spam emails on sight, to reduce everybody’s abortive time to read (permanent clearance from the Deleted Items folder will be done by the Administrator).

一見垃圾電郵就立刻刪除,以免人人都要花時間看(從刪除郵件夾永久刪除由管理員做)。 - Ignore all emails received from time to time calling for security verification regarding iTune, Apple ID, Microsoft, PayPal, HSBC, etc. since they are mostly malicious emails.

千祈不要理會不時收到的關於iTune、 Apple ID、Microsoft、PayPal、HSBC 等等要人重新輸入認證的電郵,黑郵居多。 - Do not open or save attachments received from unknown persons, and do not click open links.

不要打開或儲存來自不認識的人的附件,亦不要打開連結。

Sending emails 發送電子郵件

- bcc all outgoing emails back to our office.

發出所有電郵時,密件抄送回自己公司。 - Check that the bcc copies are received by our office to prove that the outgoing server is working.

檢查自己公司是否收到密件抄送副本,以證明發送伺服器正常工作。 - Check that there are no delivery failure message (should appear within 5 minutes) to prove that the delivery is successful.

檢查沒有發送失敗消息(應在 5 分鐘內出現)以證明發送成功。 - Handle any delivery failure immediately by contacting the intended recipient for the proper address, and re-send with a remark "Re-sent due to delivery failure", cc all others on the original email to make them know.

立即處理任何送達失敗,聯繫預期收件人以獲取正確地址,重新發送,註明“因送達失敗而重新發送”,並抄送原始電郵中的所有其他收件人以知會他們。 - For urgent email failed to be delivered after retry or failure to contact the intended recipient, fax the email copy to his/her company with a remark "Faxed due to email delivery failure" and the date. Email the front page back to the office.

緊急電郵在重試後仍未能送達或未能聯繫到預期的收件人,將電郵副本傳真給他/她的公司,並註明“因電郵送達失敗而傳真”和日期。 將首頁通過電郵發回自己公司。 - Email source files (Word, Excel, etc.) back to our office after sending out pdf files. Mark at the beginning "Source files attached".發送 pdf 文件後,將源文件(Word、Excel 等),電郵發送回自己公司。 在開頭標記“附加的源文件”。

Correspondence not by emails 非電郵的來往文件

- All outgoing and incoming documents not sent by email should be emailed back to our office for the record on the same day.

所有非通過電郵發送的來往文件應在同一天通過電郵發送回自己公司以資記錄。

Printing frequency (no longer adopted) 打印頻率(不再採用)

- Print all emails once every half-an-hour as far as possible.

盡可能每半小時打印一次所有電郵。 - Print before lunch break all emails received before 12 am.

午休前打印所有在上午 12 點之前收到的電郵。 - Print before close of a day's work all emails received before 5 pm.

在一天的工作結束前打印下午 5 點之前收到的所有電郵。 - Print upon starting a day's work all emails received before that.

在開始一天的工作時打印之前收到的所有電郵。

Persons responsible for filing emails 電郵歸檔負責人

- Be responsible for filing the softcopies of emails of their own projects.

- Assign more junior or newly joined staff members to file softcopies of emails for a team of staff members.

- Define filters.

- Clerical staff (if available):

- Assign a person as the final guard to remind all others to print their emails by the 12 am and 5 pm deadlines, and print all remaining emails not falling within the scope of the any particular team.

- The above principle still applies if a clerk is employed to do the printing.

Printing (when necessary)

- Print the newly received pages of the emails only, i.e., excluding linked pages of past emails which have been received before.

- Print on one-sided recycled paper. (One-sided printout will be easier for reading and future scanning for archiving.)

- Print on double-sided paper only when required by the surveyor responsible.

- Print the one with track-changes if both Word or Excel and pdf files are received.

Not to print

- Delete spam emails.

- Delete promotional emails not relevant to our industry, profession or business.

- Do not delete nor print promotional emails relevant to our industry, profession or business. File them under their relevant folders, if available, otherwise under "Sales Promotion".

- Permanent deletion from the Trash folders should only be made by the director.

- Do not print documents which are too thick, say more than 30 pages. Ask the surveyor responsible to see whether the thick documents should be printed.

Emailed copies of faxes

- Treat emailed copies of faxes similarly.

- Convert emailed copies of faxes to proper emails by forwarding each email with attached fax back to the office but stating a proper subject title and inserting an image of the first page in the email beforehand.

Documents sent through links

- Do not download from links sent by unknown senders for unknown purposes. Check with the senders if in doubt.

- Download ALL documents received through genuine links and and email them back to our office for the record.

- Email ALL documents sent out through links back to our office for the record.

- Split them into several emails if the file size is too large.

Emails attached to emails

- Save emails attached to an email received on to the computer desktop and move them back to the email folder. They will appear at the positions of their original email dates. This would enable reading the story in a chronological order, and easy tracing later.

- Print such emails like other emails.

Handling of printed emails

- When there are more than one attachment, identify whether they belong to one submission or several submissions each bearing its own serial number or date (e.g., letters, site memos, proposed variations, instructions, variation quotations, payments, minutes, regular reports, etc.).

- Separate between different submissions by staples or clips.

- Arrange different submissions according to the dates stated on them (not the dates received).

- Within the same submission, arrange the attachments in logical sequence, usually covering letter or site memo at the front and drawings at the back. Descriptive documents are usually in the middle. Summaries may be put before or after the details depending on the authors. Follow the specific contents page or the list of items stated in the email. Do not follow the order of the attachments to the email because they have no logical sequence.

- Fold thin A3 attachment (say, not exceeding 5 pages) forward from right to left along the centre line into A4 size, and then fold the top flap from left to right along the centre line into half A4 size.

- Fold thick A3 attachment backward from right to left keeping the edge clear from the left punch holes.

- Stamp the date received on the top right hand corner of each separate submission received (but no need for different parts of the same submission which are not supposed to be taken out for use separately).

- Stamp the date received on the top right hand corner on each programme and on the bottom right hand corner on each drawing because they may be filed or taken out for use separately.

- Mark near the date chop the relevant instruction numbers.

- Stamp neatly and clearly at a blank space.

- Do not stamp on submissions emailed by our office unless they are returned with emails received.

- Write on the emails simple reference numbers and dates of those separate submissions which are filed not immediately after the relevant emails to enable future tracing.

- Initial neatly on the bottom left corners of the emails after arranging the emails and attachments.

- File the emails directly in the appropriate email sub-folders of the relevant projects.

- If the emails are printed by somebody other than the relevant team members, file the emails under the "00Printed" email folder for subsequent filing by the relevant team members.

- Distribute the printed emails once every half-an-hour to the relevant project team members for reading.

- Circulate within the relevant team starting from the director to the assistant. If any person is absent, pass on to the next one present.

- Read and initial on the top right hand corners of the emails and the first pages of separate submissions.

- Take immediate actions as required by the emails.

- File the emails in the relevant hardcopy folder after all team members have read and initialled and when no further immediate action is required.

- File different submissions according to their dates even though those dates may be sometime in the past so that they can tell the complete story when the files are read sequentially sometime later. The date received stamp can help to trace that emails sending them though the submission and the email may be filed separately.

Filing of letters and emails 信件和電郵的歸檔

(Section added 添加, 7/7/2021)

- Create a separate folder section for each preliminary cost estimate, proposed instruction, confirmation of verbal instruction, formal instruction, other item to appear in the final account (e.g., group of provisional quantities, provisional sum), financial report, payment valuation, etc.

- Name the email folders or label the hardcopy folder flysheets by their serial numbers.

- If an email covers more than one folder section, email it back to the office with a note added to the subject so as to distinguish. Do not just make copies because identical copies will be deleted if a "remove duplicate" check is done.

- File requests for estimates and estimates under the proposed instruction folders. Move them to the formal instruction folders after the issuance of the formal instructions.

- Move confirmations of verbal instructions to the formal instruction folders after the issuance of the formal instructions.

- Change the folder or label names to reflect or track the move.

- File quotations and assessment related to a formal instruction under the same folder section, i.e., all matters related from cost estimate until agreement are to be filed together to tell the complete story.

- Spilt into more folders if an instruction covers more than one variation or final account item.

- Update the financial report descriptions and amounts to match whenever a new or revised quotation or assessment is received or issued.

- File communications with each tenderer separately. This is important for tracking the development, preparing the letter of award/intent, and contract binding.

- In principle, all incoming and outgoing documents in the email folders and hard copy folders should mirror each other, except for working documents not sent out.

- Bind tender documents as a book, not to be filed.

Quality Alerts

(Section added, 18/3/2026)

Email size limits

- Limit the total outgoing email attachment size to 7 MB because:

- Common email size limits (including attachments)

- Gmail (Personal): 25 MB

- Gmail (Google Workspace): Up to 50 MB, or 70 MB for some enterprise plans

- Outlook.com/Hotmail: 20-25 MB

- Outlook/Office 365 (Business): 35 MB (configurable up to 150 MB)

- Yahoo/AOL Mail: 25 MB

- General/ISP Email: 10 MB - 20 MB

- Recipients' email servers may have a lower limit.

- Due to encoding, files may grow by about 30%–40% when converted to email attachments.

- (Our company email size limit is 200 MB.)

- Common email size limits (including attachments)

- Compress the attachments to zip or rar formats to reduce size, but some organisations do not accept rar attachments.

- Set to output as zip format when using WinRaR.

- Use WinRaR to split compressed file into volumes (parts) to stay within the desired compressed file size limit.

- Remind users to download all volumes in order to access all the files within different volumes.

- Do not need to compress PDF files to zip or rar formats because the size reduction is small.

- Use PDF editing tools to reduce the PDF file size which can be more than a half.

- Check that the resolution after reduction is still satisfactory.

Cloud link storage

- Avoid using cloud links even though it is common to send cloud links for downloading large files.because:

- The files stored on the cloud may be changed before or after they are downloaded.

- The files actually downloaded by different users at different times may be different.

- There is no evidence to prove that the files downloaded and used are the same as those originally provided for downloading.

- Send files as email attachments as far as possible.

- Limit to use cloud link storage to really big files.

- Email back the downloaded files for record.

- Emails themselves serve as records of the times of delivery of the attachments with actual contents.

Email non-delivery

- bcc outgoing email back as a quick check to ensure successful delivery.

- Set the outgoing email server to report email non-delivery within 5 minutes so that immediate action can be taken.

- Inform the recipient in case of non-delivery, and agree alternative means of delivery.

- Re-send the email as appropriate if the email address is correct or after the full email box has spare space. Mark the email as "Re-sent due to non-delivery". Note "Re-sent", not "resent".

- In case of a change of email address, copy to other recipients as well when re-sending to keep them informed of the updated address, so that they will not reply to the previous email containing the outdated email address. Send only with all attachments to the updated email address, and send and copy to others again but without attachments in case the attachments are too large.

- Fax the undelivered email marked with "Faxed due to email non-delivery" to the recipient, if the recipient cannot be contacted.

- Mark the recipient email address as "(left)" if he or she no longer works there.

Folder management

- Use the email folders as a file managment system.

- Set up different folders for different jobs, different sub-folders for different topics, and sub-sub-folder for each estimate, instruction, payment, etc.

Documents exchanged not by emails

- Scan to PDF and email back all documents sent or received in hardcopies or faxes to ensure that the emails represents the complete file storage.

Hong Kong Quantity Surveyors and Mainland Cost Engineers 香港工料測量師及內地造價工程師

Hong Kong Quantity Surveyors and Mainland Cost Engineers 香港工料測量師及內地造價工程師 KCTangNote

18/2/2023: Updated.

11/3/2020: Updated.

20/12/2014: Moved from wiki.

Quantity Surveyor

- Is a construction cost and contract consultant.

- Originated in Britain as a profession.

Nicknames of Quantity Surveyor

- “cost engineer” as used in the mainland China and the USA.

- “construction cost manager” to recognize his expertise in managing construction costs.

- “construction contract specialist” to recognize his expertise in understanding the law of contracts, the standard forms of construction contracts, and giving advice accordingly to other project team members.

- “construction economist” to recognize his expertise in understanding construction cost factors, variables, and impacts.

- “risks manager” to recognize his ability to draft contract and cost clauses to present the risks clearly to help tenderers submit adequate prices, and reduce post contract surprise claims and disputes.

- “lubricant” (my own invention) to recognize his skill in providing fair and reasonable cost and contractual advice to resolve deadlocks which may exist between other project team members on opposite sides of the table.

Professional Bodies which include Quantity Surveyors and Cost Engineers (or their Professional Bodies) as Professional Members (not exhaustive)

- The Hong Kong Institute of Surveyors (HKIS)

- Africa Association of Quantity Surveyors (AAQS)

- Association for the Advancement of Cost Engineering International (AACE)

- Association of Cost Engineers (ACostE)

- Association of South African Quantity Surveyors (ASAQS)

- Australian Institute of Quantity Surveyors (AIQS)

- Brazilian Institute of Cost Engineers (IBEC)

- Building Surveyors Institute of Japan (BSIJ)

- Canadian Association of Consulting Quantity Surveyors (CACQS)

- Canadian Institute of Quantity Surveyors (CIQS)

- Chartered Institute of Building (CIOB)

- Chartered Institution of Civil Engineering Surveyors (ICES)

- China Cost Engineering Association (CCEA)

- Commonwealth Association of Surveying and Land Economy (CASLE)

- Conseil Européen des Economistes de la Construction (CEEC)

- Consejo General de la Arquitectura Técnica de España (CGATE)

- Dutch Association of Quantity Surveyors (NVBK)

- European Federation of Engineering Consultancy Associations (EFCA)

- Fédération Internationale des Géomètres (FIG)

- Fiji Institute of Quantity Surveyors (FIQS)

- Ghana Institution of Surveyors (GhIS)

- Ikatan Quantity Surveyor Indonesia (IQSI)

- Indian Institute of Quantity Surveyors (IIQS)

- Institute of Engineering and Technology (IET)

- Institute of Quantity Surveyors of Kenya (IQSK)

- Institute of Quantity Surveyors Sri Lanka (IQSSL)

- Institution of Civil Engineers (ICE)

- Institution of Surveyors of Kenya (ISK)

- Institution of Surveyors of Uganda (ISU)

- International Cost Engineering Council (ICEC)

- Italian Association for Total Cost Management (AICE)

- Korean Institution of Quantity Surveyors (KIQS)

- Fachverein für Management und Ökonomie im Bauwesen (maneco)

- New Zealand Institute of Quantity Surveyors (NZIQS)

- Nigerian Institute of Quantity Surveyors (NIQS)

- Pacific Association of Quantity Surveyors (PAQS)

- Philippine Institute of Certified Quantity Surveyors (PICQS)

- Property Institute of New Zealand (PINZ)

- Real Estate Institute of Botswana (REIB) Royal Institute of British Architects (RIBA)

- Royal Institution of Chartered Surveyors (RICS)

- Royal Institution of Surveyors Malaysia (RISM)

- Singapore Institute of Building Limited (SIBL)

- Singapore Institute of Surveyors and Valuers (SISV)

- Sociedad Mexicana de Ingeniería Económica, Financiera y de Costos (SMIEFC)

- Society of Chartered Surveyors Ireland (SCSI)

- Union Nationale des Economistes de la Construction (UNTEC)

Major Types of Employers of Quantity Surveyors in Hong Kong

香港顧問工料測量師的主要僱主類別

- Consultant quantity surveying practices工料測量顧問公司(as directors, partners, or quantity surveyors of different grades).

- Contractors 承建商(as directors, commercial managers, contract managers, quantity surveying managers, or quantity surveyors of different grades).

- Government, quasi-government organizations, and tertiary educational institutions 政府、半官方機構、大專院校(as directors, project managers, or quantity surveyors of different grades).

- Developers 發展商(as directors, project managers, and monitoring quantity surveyors of different grades).

Major Scope of Services of Consultant Quantity Surveyors in Hong Kong

香港顧問工料測量師的主要服務範圍

- Preparation of pre-construction cost estimates.

編訂概算 - Cost planning during the design stage.

設計階段造價控制 - Preparation of tender documents.

編訂招標文件 - Pre-qualification of tenderers.

投標單位預審 - Tender analysis.

審標 - Tender negotiation.

議標 - Contract award.

定標 - Preparation of contract documents.

編訂合同文件 - Checking of insurance policies and performance bonds.

審核保險單、履約保證書 - Valuation of progress payment applications.

審核進度款 - Cost monitoring during the construction stage.

施工階段造價控制 - Valuation of amounts of variations and claims.

審核變更費、索賠 - Negotiation and agreement of final accounts.

商議結算

Specialized Services of Some Consultant Quantity Surveyors in Hong Kong

香港某些顧問工料測量師的特別服務範圍

- Claims consultancy.

索賠顧問 - Dispute resolution advisory, mediation and arbitration.

解決爭議、調解、仲裁 - Insurance loss adjustments.

保險理賠 - Facilities management.

設施管理 - Value management.

價值工程 - Partnering facilitation.

促進夥伴關係

Areas of Specialization as written by HKIS

- Please check https://hkis.org.hk/en/division_qsd.html?id=101

Characteristics of Consultant Quantity Surveyors in Hong Kong

香港顧問工料測量師的特色

- Full services from inception of project to completion of construction and defects rectification.

由項目構思到建造完成的全過程造價諮詢服務 - Now extending to post completion maintenance until redevelopment.

現在申延到建造後的維修直至重建 - Dynamic management with constant review and updating.

不斷檢討及更新的動態管理 - Cost and contract management of various kinds.

造價及合同管理多樣化 - Self-regulated by professional bodies.

自我約制(通過專業團體) - No Government control, though there is a Surveyors Registration Ordinance.

沒有政府監管(雖然有測量師註冊條例) - Mainly handling contracts with Bills of Quantities, but also contracts without Bills of Quantities.

主要處理有工程量清單的合同,但亦處理沒有工程量清單的合同

Major Scope of Services of Contractor Quantity Surveyors in Hong Kong

香港承建商的工料測量師的主要服務範圍

- Similar to that described for Consultant Quantity Surveyors but starting from the tender stage.

與顧問工料測量師的差不多但從投標階段開始 - Essentially commercial and contract management for the contractors.

主要負責承建商的商務及合同管理 - Dealing with upstream clients and consultants.

處理上游的委託方及顧問 - Dealing with downstream sub-contractors, suppliers and workers.

處理下游的分包商、供應商及工人

Surveyors Registration Ordinance

- There is a Surveyors Registration Ordinance with a Surveyors Registration Board set up to register professional surveyors.

- Surveyors so registered are entitled to be called “Registered Professional Surveyors” such as “Registered Professional Surveyors (Quantity Surveying)”.

- Such title is required for undertaking outsourced Government projects but is not mandatory for civil servants or working on private projects.

Getting professionally qualified

- Typically, a person has to possess the required academic qualifications, apply to become a probationer of the professional institute, undertake a prescribed period of training and pre-qualification structured learning (PQSL), and submit to assessment of professional competence (APC) before being eligible to apply for full membership.

- Please check https://hkis.org.hk/en/membership_become.html for HKIS membership.

- Please check https://hkis.org.hk/en/membership_routes.html for HKIS routes to membership.

- Please check https://hkis.org.hk/en/professional_apc.html?division=QSD&S=5 for HKIS APC.

- Please check https://www.rics.org/en-hk/surveying-profession/join-rics/ for joining RICS.

Training Path of a Typical Consultant Quantity Surveyor

- Join a consultant quantity surveying practice.

- Check the arithmetic of calculations done by others.

- Measure quantities for approximate cost estimates, bills of quantities, variations, and remeasurement.

- Get to know the Standard Method of Measurement better throughout the process.

- Get to know the geometric forms and names of the components making up the whole construction.

- Draft bills of quantities for editing by the senior.

- Participate in counter-checking the measurement done by team members.

- Assist in monthly valuation of contractors’ payments.

- Visit the site for the purposes of doing the valuation.

- Assist in preparing monthly financial reports.

- Accompany the senior to attend pre-contract design meeting or post contract site meetings.

- Price the variations and remeasurement.

- Price the approximate cost estimates and the bills of quantities.

- Agree final accounts with the contractors.

- Assist to prepare the comparison tables attached to tender reports.

- Assist to checking the typo corrections of tender documents drafted by the senior.

- Assist to draft tender documents.

- Assist to comment on insurance policies and bonds.

- Attend meetings independently.

- Give advice on tendering procedure, contractual arrangement and choices of contract clauses.

- Draft tender documents independently.

- Interview tenderers.

- Prepare tender reports independently.

- Supervise assistants.

- Perform independently.

- Continue to give advice on post contract contractual issues.

- Help avoid and resolve disputes.

Personal Attributes

- Fair and reasonable – While Consultant Quantity Surveyors are engaged by their clients to protect the clients’ interest under the construction contract, they also have a duty under the construction contracts to act fairly and reasonably. Being fair and reasonable can in fact avoid unnecessary disputes under the construction contracts.

- Integrity – Quantity Surveyors are dealing with money though no money is actually passing through him. However, any corruptive act would mean a huge sum of money lost by the clients or contractor-employers. Quantity Surveyors must serve with the highest degree of integrity.

- Patience and persistence – Quantity Surveyors need to spend a long period of time to measure the quantities required for bills of quantities time and again. This would need patience and persistence to the task. Quantity Surveyors have to negotiate with contractors over contractual and monetary claims. Differences in opinions can lead to heated arguments. Patience is again very important.

- Attention to details – Quantity Surveyors must be accurate in his words and cost figures. Great attention to details to ensure error free is a must. Self-checking and cross-checking are both essential.

(updated, 18/2/2023)

Core Skill-sets Required

- Construction technology - Good knowledge of construction technology is the foundation stone of any surveyors.

- Building services – While traditionally cost management of building services is handled by the building services engineers, for over 3 decades in Hong Kong Quantity Surveyors have already been providing measurement and cost management services for building services. Therefore a good knowledge of building services is also required.

- Mathematics – Daily life mathematics is enough. Use of calculus is rare.

- 3-D visualization – Quantity Surveyors should be able to visualize the 3-dimensional geometry based on 2-dimensional drawings.

- Measurement – Good measurement knowledge and skill are the next higher level of foundation stone of Quantity Surveyors.

- Language – Quantity Surveyors have to read many documents ranging from Standard Method of Measurement, Specifications, Forms of Contract, legal textbooks, occasionally case laws, insurance policies and bonds. Quantity Surveyors have to draft terms and conditions into the tender documents for construction contracts and loopholes must be avoided. Consultant Quantity Surveyors have to write to advise their clients and other members of the consultant teams. Contractors’ Quantity Surveyors must also be able to write properly to put forward the Contractors’ case. The language skills of Quantity Surveyors must be high in order to rise up the career ladder.

- Use of computers and software – Quantity Surveyors have to know how to use the usual office automation software with proficiency.

- Site visit – Quantity Surveyors should like to go to site periodically.

(updated, 18/2/2023)

Valued Added Skill-sets

- Building Information Modelling – This is an important technology which must be learned and used by the present-day construction related professionals. Some Quantity Surveyors have developed special interest to realise the potential of BIM for Quantity Surveyors.

- Software programming skills – While the majority of Quantity Surveyors do not have the need and therefore the aptitude to possess software programming skills, better use of BIM requires the knowledge to write scripts or programmes.

- Digital transformation – Transforming and running the business work flow and deliverables in digital mode are the upcoming trend of all business sectors. Quantity Surveyors cannot fall behind.

- Carbon emission reduction – Calculating carbon emissions and formulating carbon emission reduction measures will be the required upcoming skills of Quantity Surveyors.