Estimating and Pricing

Estimating and Pricing KCTangNote

- 20/2/2023: Split into various pages.

- 18/2/2023: Revised.

- 7/3/2022: Cost geometry and most significant cost parameters moved from Pre-Contract Cost Planning and Control.

- 17/2/2021: Term contract edition updated.

- 17/3/2020: Revised.

- 26/2/2020: Revised.

- 17/2/2020: Tender price indices links updated.

- 20/12/2014: Moved from wiki.

Rates and Prices

Rates and Prices KCTangNote

- 20/2/2023: Split from "Estimating and Pricing". Incorporating mark-up, margin, wastage, bulkage and shrinkage.

Cost and price

- “Cost” and “Price” are often used interchangeably.

- Between the two parties to a transaction, the price quoted by the Seller / Contractor is the cost to the Buyer / Employer / Client.

- For the same party, Cost + Profit = Price.

- Seller's price = buyer's cost.

Values

- Values can be monetary prices or other benefits.

- Cost can also include non-monetary costs.

Price build-up

- The total price is built up from:

Labour costs (人工費)

+ Material costs (材料費)

+ Plant costs (機械費)

Direct costs (直接費)

+ Site and project overheads (現場及項目管理費)

+ Head office overheads (公司管理費)

Costs (成本)

+ Profit and risks allowance (利潤及風險費)

All-in price before value added tax (稅前綜合價)

+ Value added tax (從價稅)

All-in price (稅後綜合價)

- The value added tax here means a tax chargeable upon the net total price before this tax or the gross total price after this tax. Hong Kong does not implement valued added tax. Hong Kong only charges profit tax on the realisable profit annually.

- Some of the site and project overheads are not directly related to a particular work item but are commonly shared by more than one item. It is normal to price for these site and project overheads as the Preliminaries. The all-in rate for the work item will then only include the balance of the site and project overheads not included in the Preliminaries.

- Profit and overheads are usually allowed for as a percentage of the direct costs. The usual norm for variation is 15%, but it will be very different in competitive tenders. The profit and overheads allowed in the prices for different items can be different.

- Some part of the Works may be sublet to sub-contractors. They will include their own overheads in their prices to the Contractor. They may also share to provide some of the site overheads otherwise provided by the Contractor. Therefore, the mark-up on sub-contractors' prices for profit and overheads should be less than that on direct labour and materials.

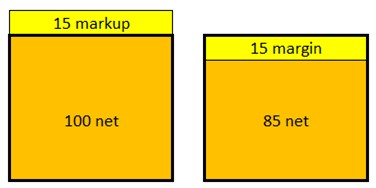

Mark-up and margin

- 100 x (1 + 15%) = 100 + 15 = 115:

- 115 has a mark-up of 15%.

- 85 + 15 = 100:

- 100 has a margin of 15%.

- 15/115 = 13.04%:

- A mark-up of 15% is equal to a margin of 13.04%.

- 15/85 = 17.64%:

- A margin of 15% is equal to a mark-up of 17.64%.

(revised, 18/2/2023)

Cost, price, profit, mark-up and margin

- Simple approach:

- When we face with the above terms, what should be the mathematical formulae to handle them and how can we remember the formulae?

- Instead of using x, y and z to represent the formulae, it would be easier to derive the formulae based on some simple numerical values using 100 as the base.

- cost + profit = price.

- profit markup % = profit / cost x 100%.

- profit margin % = profit / price x 100%.

- Given profit markup and price, how to get the cost?

- A long way:

- Cost + cost * profit markup % = price

- Cost * (1 + profit markup %) = price

- Cost = price / (1 + profit markup %) = price x 100 / (100 + profit based on 100).

- A quicker way:

- If cost = 100 and profit markup = 15%, then profit = 15 and price = 115

- This means, cost = price x 100 / 115

- If cost = 100 and profit markup = 10%, then profit = 10 and price = 110

- This means, cost = price x 100 / 110

- To conclude, if profit markup = P%, then cost = price x 100 / (100 + P).

- If cost = 100 and profit markup = 15%, then profit = 15 and price = 115

% wastage

- If a finished qty of work of 100 requires a material qty of 120. The qty wasted is 20.

- Should the wastage be 20/100 = 20% or 20/120 = 16.67%?

- Both can be correct depending on which is used as the base.

- However, in pricing, when the payment is based on the finished qty, the qty wasted should be borne by the finished qty.

- In the above example, the addition to cover the qty wasted is 20/100 = 20%, so the wastage should be 20%.

- If a 3 x 6 finished board requires a 4 x 8 uncut board, the wastage to be allowed is (4 x 8) / (3 x 6) - 1 = 32/18 - 1 = 77.78%.

- To conclude, the wastage to be allowed

= qty wasted / finished qty

= (qty used - finished qty) / finished qty

= (qty used / finished qty) - 1. - The denominator is the payable qty (finished qty).

% bulkage (excavation)

- How to allow for the extra volume to work on if payment is based on the volume before bulking?

- Bulkage or bulking factor = volume after bulking / volume before bulking.

- Volume after bulking = volume before bulking x bulkage.

- The addition to cover the extra volume is volume before bulking x bulkage. This should be simple.

% shrinkage (concrete, mortar, plaster, screed) or % compaction (soil backfilling)

- How to allow for shrinkage if payment is based on the quantity after shrinkage?

- If shrinkage = 20%, for each 100 qty, qty shrunk = 20, qty left = 80.

- The addition to cover the qty shrunk = 20/80 = 25%.

- If shrinkage = 30%, for each 100 qty, qty shrunk = 30, qty left = 70.

- The addition to cover the qty shrunk = 30/70 = 42.86%.

- If shrinkage = S%, then the addition factor = S/(100-S).

- The denominator is the payable qty (qty left).

All-in rates and unit of quantity

- All-in rate = all-in price / quantity.

- Not all the costs are directly proportional to the quantity of the work, it can be a combination of:

- Variable costs

- Fixed costs.

- Cost = f(weight) + f(volume) + f(area) + f(length) + f(number) + f(quality) + f(quality) + f(time) + f(others).

- When the total price of a work item is required to be broken down into quantity and rate, the unit of the quantity to be used should be one which represents the most cost significant variable.

- If there are more than one cost significant variable, then the work item should be broken down into more than one sub-item.

- It is usual and easier to estimate the cost of a bigger sample quantity of a work item first and divide the cost by the quantity to obtain the unit rate so that:

- Those costs not directly related to the quantity of the work item can be shared

- Wastage, laps, etc. which are not measured in the quantity can be allowed for.

(revised, 18/2/2023)

Rate build-up

- Labour costs:

- Daily rates to include for:

- daily basic wage

- travelling and meal allowances

- allowances for hand tools and personal accessories

- allowances for holidays with pay

- mandatory provident fund (MPF) contribution

- year end bonus

- incentive payments

- levies and insurances if not priced separately

- etc.

- Time to consider:

- taking from stores, hoisting, lowering

- placing, fixing

- non-productive travelling and recess time

- etc.

- Daily rates to include for:

- Material costs:

- Rates to include for:

- ex-factory costs, package

- export transportation, transit insurance

- customs clearance and duties

- demurrage, off-site storage

- local delivery

- off-loading, returning package

- etc.

- Quantities to consider:

- basic quantities

- breakage, damage, theft

- wastage (cutting, conversion)

- unmeasured laps

- bulkage, consolidation, shrinkage

- etc.

- Rates to include for:

- Plant costs (called "Equipment costs" in civil engineering contracts):

- Rates to include:

- Use of plant (not purchasing of plant)

- Mobilization, relocation and demobilization costs, if not measured separately

- Fuels and consumables

- Maintenance and repair.

- Time to consider:

- Time used

- Unavoidable idling time

- Mobilization, relocation and demobilization time, if not measured separately.

- Rates to include:

- Site and project overheads

- Expenses on site or off-site specifically due to the project, not specifically related to any particular group of work but are commonly shared.

- Head Office Overheads

- Expenses in running the head office, shared between different concurrent projects.

- Profit

- The expected profit with allowance for risks.

- Tax if charged based on total price (not in Hong Kong which implements profits tax on the realisable profit annually, not value added tax on turnover).

- Rates build-up applicable to measured work as well as preliminaries.

Tender pricing

See Tender Pricing for more details.

Consultants' Cost Data

Consultants' Cost Data KCTangNote

- 24/12/2024: "Price information" moved from "Quality Alerts".

- 20/2/2023: Split from "Estimating and Pricing".

Price information

價格資訊

- Build-up a database.

建立資料庫。 - Collect directive circulars and prices published by Government and authorities.

收集政府、權力機構的指令性通知、價格。 - Collect market prices from other commercial sources (e.g., cost software vendors).

收集其他商業渠道的市場價格(例如造價軟件公司)。 - View newspapers, periodicals, internet.

檢閱報章、期刊、互聯網。 - Enquire market prices from prospective contractors, sub-contractors and suppliers.

向潛在承包商、分包商和供應商詢問市場價格。 - Collate internal information.

整理自身的資料。 - Analyse content ratios and unit costs of past projects.

分析過往工程含量及單位造價。 - Obtain through tendering.

通過招投標取得。

(Written on 4/11/2015 and moved from "Quality Alerts"; 4/11/2015初寫,從"質量提示"搬過來, 24/12/2024)

Consultants' source of data

- Tenderers when tendering will get their cost data by making enquiries with their prospective sub-contractors and suppliers.

- Consultants may make enquiries with prospective contractors, sub-contractors and suppliers for cost data but may only be able to obtain some indicative budgetary prices which may differ from that obtained under circumstances of real business opportunity and competitive tendering.

- To evaluate whether tender prices received are reasonable market rates, other cost data not received for the same tender would need to be used to compare.

- Consultants would therefore rely more on past cost data for cost estimating and for evaluation of tenders.

- Consultants would know the rates and prices in tenders received but would not normally know the costs, profit and overheads in the tenders. It does not really matter when the Consultants are interested more on the all-in rates. The details of costs, profit and overheads are only essential when handling claims.

- When estimating composite rates covering more than one work item, the quantity ratios of the constituent work items would be important.

- Rates:

- Tender prices

- Final Account prices

- New inquiries (contractors, sub-contractors, suppliers)

- Architectural Services Department Schedule of Rates for Term Contracts for Building Works 2019 Edition:

- https://www.archsd.gov.hk/media/publications-publicity/schedule-of-rates/sor2019_vol_1_bw_2.pd

- https://www.archsd.gov.hk/media/publications-publicity/schedule-of-rates/sor2019_vol_2_bs_2.pdf

- They are published once every many years and should be used with extreme caution for new works.

- Quantity factors and ratios:

- Cost Analyses of Other Projects

- Analyses by sampling.

Adjust for time differences

- There can be up or down fluctuations of costs and prices over time. When using past cost data for the present or future work, adjustments should be made for the time differences.

- Indices for adjusting for time differences:

- Cost indices – reflecting labour and material costs

- Tender price indices – reflecting prices of work

- Consumer price indices – reflecting general consumer prices not just for the construction industry.

- Cost indices and tender price indices can change at different rates. Cost indices can rise but tender price indices may fall in case of severe competitive market lacking work.

Index references

- Census and Statistics Department - Index Numbers of the Costs of Labour and Materials used in Public Sector Construction Projects

- Census and Statistic Department - Average Wholesale Prices of Selected Building Materials

- Architectural Services Department - Building Works Tender Price Index

- Architectural Services Department - Building Services Tender Price Index

- Rider Levett Bucknall Construction Cost Update Hong Kong

- Arcadis Quarterly Construction Cost Review Hong Kong and China

Cost Geometry 造價幾何

Cost Geometry 造價幾何 KCTangNote

- 27/2/2023: Revised.

- 20/2/2023: Split from "Estimating and Pricing".

Cost vs quantity

Not a straight-line relationship between costs and quantities

- Cost = f(weight) + f(volume) + f(area) + f(length) + f(number) + f(quality) + f(quality) + f(time) + f(others).

- But, the pricing unit of an item of work or material is based on one kind of unit of measurement.

- This means that all other costs not related to that unit have to be converted to use that unit as the base.

- These other cost factors do not change in direct proportion to the pricing unit.

Total cost vs quantity

- The total cost of factory production (and therefore sales of materials and goods) does not increase in proportion to the increase in the quantity produced, since there are some initial fixed costs (e.g. factory, equipment, rental deposits) and recurring fixed costs (e.g. monthly rents, additional equipment when the existing capacity is exceeded) not in proportion to the quantity to be included.

- The total sales value may also not increase in proportion to the increase in the quantity sold (e.g. bulk discount, delivery vehicle not used to full capacity).

- The total cost is usually higher than the total sales value initially, but the total sales value must rise up to exceed the total cost eventually for the business to be viable.

Linear items

- For linear items, there can be fixed costs which do not change when the length changes.

- The unit rate per length can decrease if the length is increased without any change to the fixed components.

- e.g. 10 m @ $4/m + 2 No. @ $5/No. = $40 + $10 = $50;

- $50 / 10 m = $5.00/m;

- while 15 m @ $4/m + 2 No. @ $5/No. = $60 + $10 = $70;

- $70 / 15 m = $4.67/m.

- e.g. 10 m @ $4/m + 2 No. @ $5/No. = $40 + $10 = $50;

(revised, 18/2/2023)

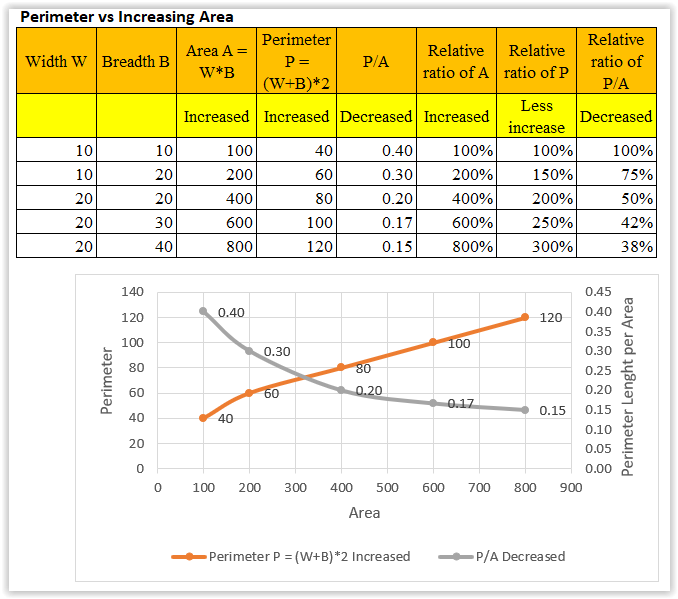

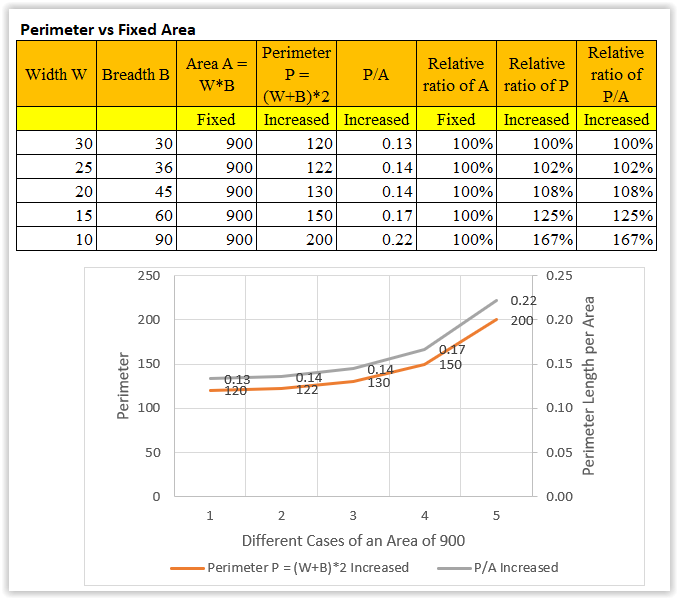

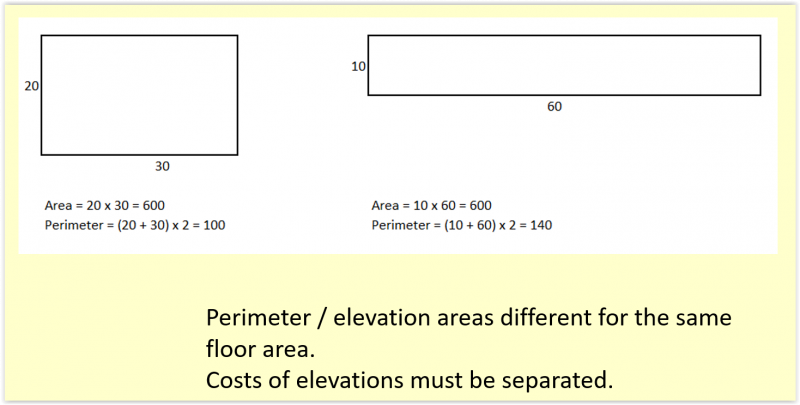

Superficial items

- For superficial items, the perimeter length increases less rapidly than the increase in the superficial area (300% vs 800% in the table below):

- The ratio of perimeter length / area decreases if the area is increased.

- This means the unit rate per superficial area would have the same effect.

- However, for the same area, the perimeter length can increase considerably if the shape is elongated:

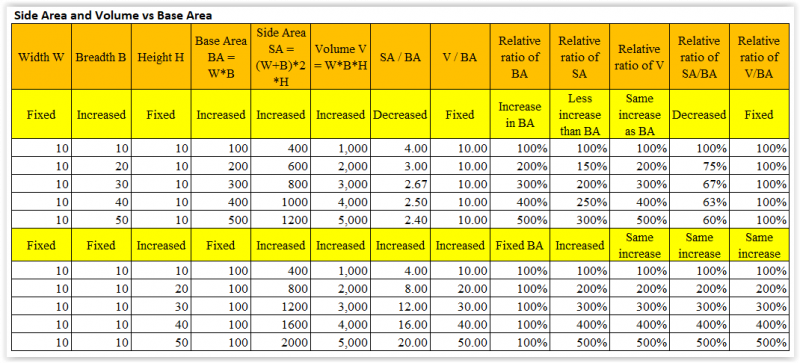

Cubic items

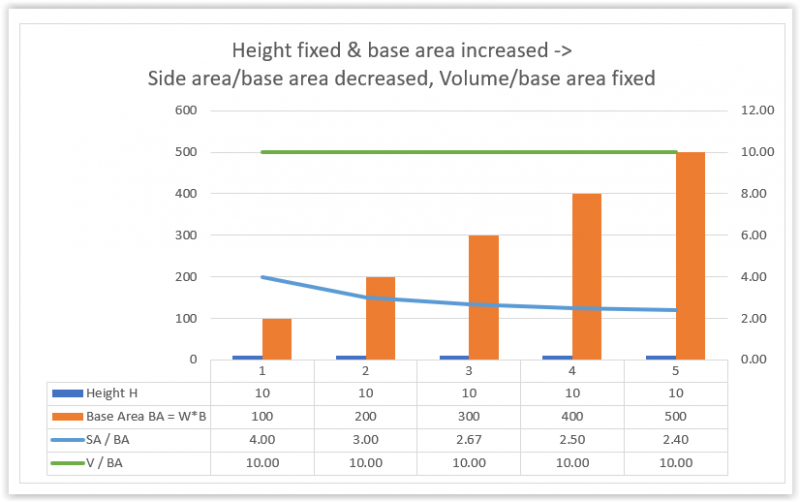

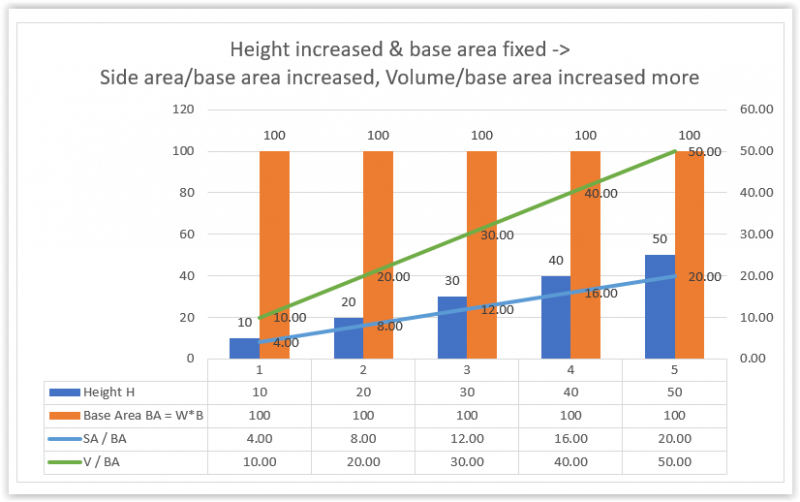

- For cubic items, the rates of change of the side area and volume relative to the base area would depend on which dimension is changed:

- For the same height, the volume increases in proportion to the increase in the base area (i.e. fixed volume/base area), while the side area increases less rapidly resulting in a decrease in the side area/base area ratio:

- For the same base area, the side area and volume increase in proportion to the increase in the height (as shown in the graph below). Their rates of change are the same:

- If both the height and the base area are increased, the volume/base area will increase, but whether the side area/base area will increase or decrease will depend on the relative rates of changes of the height and the base area.

- In all cases, the unit cost and unit sales value should therefore not remain constant.

- The appropriate unit cost and unit sales value should be determined based on the quantity required, and suitably adjusted in case of changes in the quantity.

(table added, 27/2/2023)

Impact on unit cost and unit rate

- Making a unit rate competitive enough to secure sales volume and produce profit is important.

- Works or sales contracts usually require the unit rates to be fixed even though the quantities may be varied. If the variation is significant, there can be a huge loss or profit. Some contracts permit the adjustment of the unit rates in case of unexpected big changes.

- The quantity of any item of work can vary between different construction projects and how to estimate an appropriate unit rate is crucial.

Breakdown into more or less items

- It would be more expedient if less items need to be measured to arrive at the total cost or price.

- This means that the unit rate has to allow for the costs of other related items not measured separately.

- However, when the costs of other related items do not vary in proportion to the quantity of the item measured, the unit cost of the item measured would change significant to become unrealistic, then such other related items should be measured separately for costing.

- Therefore, the unit rates should only be required to include for related items which change in proportion to the quantity measured or for non cost significant ancillary items. Yet, significant changes to the quantity may still make the non cost significant ancillary items to become significant. This is an area for contractual claims.

Building form and shape

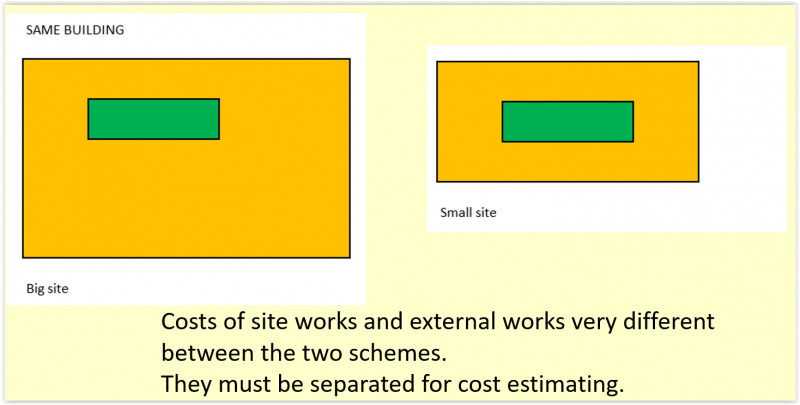

- Appreciate the effect of different site areas for the same building:

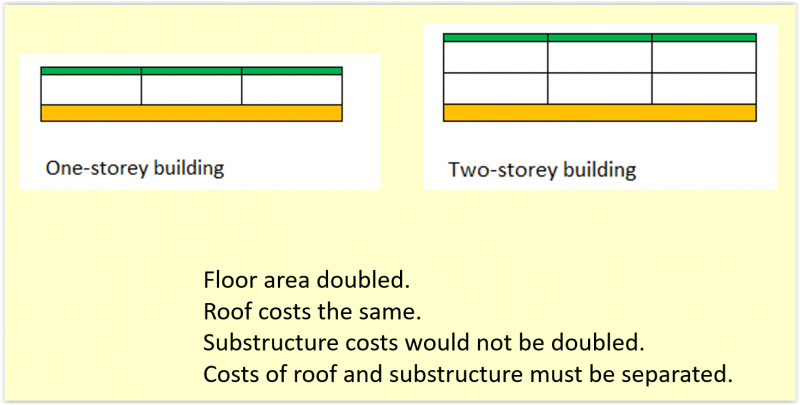

- Appreciate the effect of doubling the number of storeys:

- Appreciate the effect of elongating the building without increasing the floor area:

- Unit cost per floor area:

- Construction costs are usually compared based on unit cost per floor area.

- The above suggests that the unit cost per floor area cannot be a constant for the same type of buildings of different forms and shapes.

- Impact on design:

- The relationship of number, length, area and volume is more important for the design of the building form and shape.

- Whether a building is more economical or expensive than the other for the same floor area and type would primarily depend on the ratios of the numbers, lengths, areas and volumes of the building components to the floor areas, and then on the materials and standards.

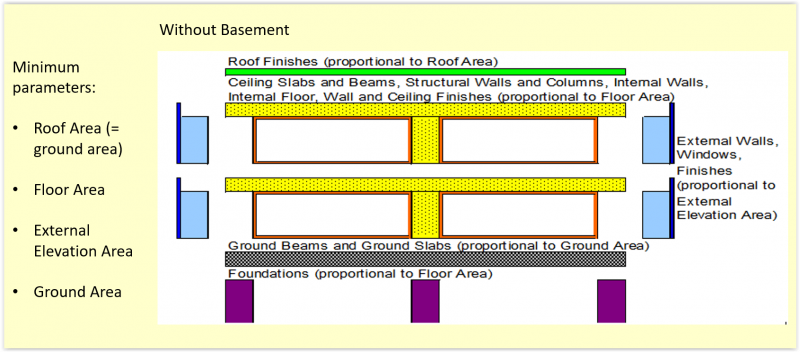

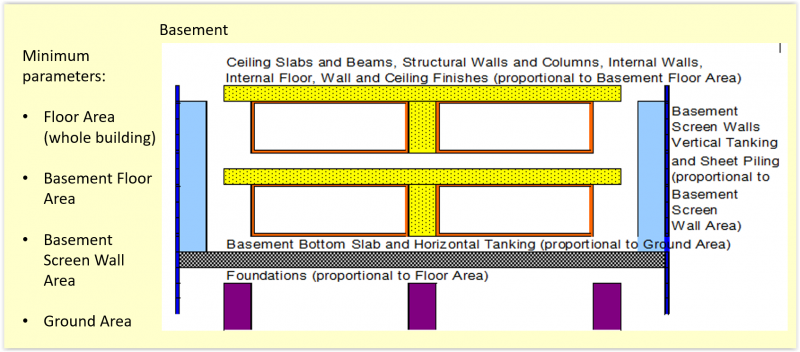

Most significant cost parameters

- Appreciate which cost portions should bear more direct proportions to each parameter:

瞭解那部份的成本內容與那個造價參數有較直接的比例關係:

- Parameters:

- Floor area (above ground + below ground)

樓面面積 - Ground area (= roof area)

地面面積 (=屋面面積) - Transfer structure area

轉換結構面積 - External elevation area

外立面面積 - Basement screen wall area or more effectively basement volume of excavation

地下室外牆面積或較有效的地下室土方體積 - Site area

工地面積 - External area (site area - ground area)

室外面積 - Number of equipment

台數 - Refrigeration tonnage

冷噸 - Other elemental quantities.

其他功能分部工程量。

- Floor area (above ground + below ground)

- Quick cost estimating:

- Using this small number of cost parameters can enable quick cost estimating.

- Accurate measurement:

- The values (quantities) of those parameters which will be used extensively throughout a cost estimate should be accurately measured, unlike the general message here that the cost estimates should be approximate.

Cost Factors

Cost Factors KCTangNote

- 20/2/2023: Title changed.

- 18/2/2023: Revised.

- 3/3/2022: Modular integrated construction added.

- 29/3/2021: Full stops added.

- 2/3/2021: Revised.

- 17/3/2020: Created.

Generally

- Cost factors may be asked from different perspectives at different stages:

- Feasibility study before choosing site:

- What type of development?

- Which country and place to invest and develop?

- Why cost differently between countries, places and sites?

- Planning and design after fixing site:

- What design, provisions, types, standards of the whole and its components?

- Why cost differently?

- Tendering:

- Why tender prices so different?

- Construction:

- Why original contract sum changes?

- Feasibility study before choosing site:

- Cost factors generally:

- Some factors affect the quantities, and therefore the total cost.

- Some factors affect the unit cost per area or unit cost per length (e.g., roads, rails, tunnels, bridges, etc.).

- Some factors affect the unit rate per quantity of work.

- Price changes during the post contract stage are excluded here.

- Think and brainstorm:

- The factors can equally apply to other industries or commercial or even social sectors.

- Common sense knowledge is to be applied.

- Classify systematically:

- There is no absolute answer to "which classification is the best?".

- A systematic classification should help people think further systematically in the future and present the more relevant factors systematically depending on the perspective and stage.

(3 and 4 added, 2/3/2021)

No fixed prices

- One important thing to learn is that there is no fixed (constant) set of unit prices in any economy, as evidenced by the many factors suggested.

- Free market economies operate on free market competition of the prices. They would only regulate prices for using government services and some public utility services.

- The mainland, China used to fix a constant set of unit prices (by issuing standard price books) with moderate periodic inflationary adjustments but when foreign materials and equipment using foreign currencies are involved, the price fluctuations can become serious. After opening up the market, the mainland has admitted significant free market competition though some measures to regulate the prices are still implemented.

- Hong Kong operates as a free market economy. Therefore, there is no fixed set of unit prices for construction works. An exception to this is that Hong Kong Government publishes Schedule of Rates for term contract works. See notes at the end.

(Section added, 2/3/2021)

Reasons for variances in unit rates in the same city

- Even for work items of the same description, the rates can be quite different between projects due to various reasons.

- Design:

- Functions

- Materials and construction

- Standard.

- Site location:

- Transportation

- Restrictions.

- Construction:

- Project size

- Extent of mechanization

- Extent of standardization

- Extent of repetition

- Extent of pre-fabrication

- Volume of bulk purchasing

- Workmanship

- Weather

- Extent of safety measures

- Extent of environmental protection measures.

- Economic environment:

- Level of market competition

- Exchange rates

- Time differences.

- Contractual:

- Degree of contractual risks

- Harshness of contract terms

- Payment terms

- Degree of design liability and statutory submission obligations

- Extent of warranties.

- Human factors:

- Consultants’ attitude

- Owners and occupiers’ attitude and co-operation

- Tenderers’ pricing strategy in distributing the costs, profit and overheads differently across different work sections.

(Section added, 2/3/2021)

Country (assuming putting a done design to a different country)

- Different planning and design regulations.

- Different environmental requirements.

- Different tax requirements.

- Planned economy or free market economy.

- Significance of government intervention.

- Different purchasing power of local currencies.

- Availability of foreign currencies.

- Availability of local supply of labour, materials, plant and management.

- Degree of reliance on foreign supply of labour, materials, plant and management.

- Different requirements on holidays and restriction on working hours.

- Different productivity of local labour.

- Different extent of availability of public roads and utilities.

- Different degree of ease of evacuation of existing occupiers.

- Significance of corruption.

Site location and conditions

- Extreme climatic conditions: hot, cold, frozen work period, typhoon.

- Seismic zones.

- Existing status of use: greenfield or brownfield.

- Existing type of use: urban, rural or agricultural.

- Existing site topography: flat, hilly, mountainous, offshore, etc.

- Ground conditions: soft, rocky, reclaimed, submerged, swampy.

- Obstructions underground and above-ground.

- Availability of public roads and utilities.

- Ease of evacuation of existing occupiers.

- Congested site or sufficient space for storage and maneuvering.

Planning and design

- Functional type of the building or civil engineering construction.

- Class and standard of the construction.

- Planning and design regulations for different sites and constructions.

- Environmental requirements.

- Structural form of the construction (brick, reinforced concrete, steel, timber, composite).

- Plan shape of the construction. (Different elevation area to floor area ratios. Square building costs less than rectangular building on external elevations.)

- Storey height. (Storey height will affect the vertical elements of the building both internally and externally. Higher storey height will increase the volume of the building to be heated or cooled, and therefore HVAC services.)

- Number of storeys. (Different shares of the roof and ground slab and beam costs. Need to have staircases for non-single storey buildings. Need to have lifts and refuge floors for tall buildings.)

- Height of the construction. (Heavier loading on taller buildings.)

- Orientation of the construction. (Thermal transmission on external surfaces. Use of sunlight.)

- Impact on neighbouring properties.

- Extent of provision of construction components.

- Functions, materials and quality of components.

- Extent of site works and external works shared by the main construction (affecting unit cost per area or length).

Economic environment

- Stability of economy.

- Forecast of cost fluctuations.

- Level of market competition.

- Exchange rates and their changes.

- Time differences (if compared between projects at different times).

Construction

- Project size.

- Period of construction and its reasonableness.

- Ease of transportation.

- Access restrictions.

- Changing labour, material and plant costs over time.

- Extent of plant required and availability of plant.

- Availability of supervisory staff.

- Extent of hoardings, covered walkways, scaffolding required.

- Extent of temporary works required.

- Extent of safety measures required during construction.

- Extent of environmental protection measures required during construction.

- Extent of mechanisation.

- Extent of standardisation.

- Extent of repetition.

- Extent of pre-fabrication.

- Volume of bulk purchasing.

- Workmanship expected.

- Weather which may be encountered.

- Availability of temporary water and electricity.

- Risks of safety, health, environmental hazards.

- Risks of changing government policies and neighbourhood and social expectations.

Contractual

- Procurement method.

- Degree of contractual risks.

- Harshness of contract terms.

- Payment terms.

- Degree of design liability and statutory submission obligations.

- Extent of insurances, bonds and warranties.

Tenderers' ability and perception (causing differences in tender rates)

- Labour, material and sub-contract costs which can be sourced at the time of tendering.

- Availability of plant.

- Availability of supervisory staff.

- Availability of expertise.

- Availability of sufficient cash flow or reliance on loans.

- Reasonableness of the period of construction.

- Consultants’ attitude.

- Owners and occupiers’ attitude and co-operation.

- Tenderers' profit expectations.

- Tenderers’ pricing strategy in distributing the costs, profit and overheads differently across different work sections.

How about modular integrated construction?

- Designers’ capabilities.

- Statutory requirements.

- Factory capabilities.

- Early involvement of contractors.

- Off-site costs, delivery and logistics, factory’s environmental impact.

- On-site storage, hoisting, special jointing, fixings, weatherproofing, fire-resistance.

- Shortened period of site overheads.

- Local environment impact.

- Local workers’ prospect.

Estimating for Building Renovation Works

Estimating for Building Renovation Works KCTangNote

- 30/6/2026: Created for HKIS BSD PQSL Event of the same title on the same day. The contents are collated from other web pages.

Rates and Prices

Cost and price

- “Cost” and “Price” are often used interchangeably.

- Between the two parties to a transaction, the price quoted by the Seller / Contractor is the cost to the Buyer / Employer / Client.

- For the same party, Cost + Profit = Price.

- Seller's price = buyer's cost.

Values

- Values can be monetary prices or other benefits.

- Cost can also include non-monetary costs.

Price build-up

- The total price is built up from:

Labour costs (人工費)

+ Material costs (材料費)

+ Plant costs (機械費)

Direct costs (直接費)

+ Site and project overheads (現場及項目管理費)

+ Head office overheads (公司管理費)

Costs (成本)

+ Profit and risks allowance (利潤及風險費)

All-in price before value added tax (稅前綜合價)

+ Value added tax (從價稅)

All-in price (稅後綜合價)

- The value added tax here means a tax chargeable upon the net total price before this tax or the gross total price after this tax. Hong Kong does not implement valued added tax. Hong Kong only charges profit tax on the realisable profit annually.

- Some of the site and project overheads are not directly related to a particular work item but are commonly shared by more than one item. It is normal to price for these site and project overheads as the Preliminaries. The all-in rate for the work item will then only include the balance of the site and project overheads not included in the Preliminaries.

- Profit and overheads are usually allowed for as a percentage of the direct costs. The usual norm for variation is 15%, but it will be very different in competitive tenders. The profit and overheads allowed in the prices for different items can be different.

- Some part of the Works may be sublet to sub-contractors. They will include their own overheads in their prices to the Contractor. They may also share to provide some of the site overheads otherwise provided by the Contractor. Therefore, the mark-up on sub-contractors' prices for profit and overheads should be less than that on direct labour and materials.

Mark-up and margin

- 100 x (1 + 15%) = 100 + 15 = 115:

- 115 has a mark-up of 15%.

- 85 + 15 = 100:

- 100 has a margin of 15%.

- 15/115 = 13.04%:

- A mark-up of 15% is equal to a margin of 13.04%.

- 15/85 = 17.64%:

- A margin of 15% is equal to a mark-up of 17.64%.

Cost, price, profit, mark-up and margin

- Simple approach:

- When we face with the above terms, what should be the mathematical formulae to handle them and how can we remember the formulae?

- Instead of using x, y and z to represent the formulae, it would be easier to derive the formulae based on some simple numerical values using 100 as the base.

- cost + profit = price.

- profit markup % = profit / cost x 100%.

- profit margin % = profit / price x 100%.

- Given profit markup and price, how to get the cost?

- A long way:

- Cost + cost * profit markup % = price

- Cost * (1 + profit markup %) = price

- Cost = price / (1 + profit markup %) = price x 100 / (100 + profit based on 100).

- A quicker way:

- If cost = 100 and profit markup = 15%, then profit = 15 and price = 115

- This means, cost = price x 100 / 115

- If cost = 100 and profit markup = 10%, then profit = 10 and price = 110

- This means, cost = price x 100 / 110

- To conclude, if profit markup = P%, then cost = price x 100 / (100 + P).

- If cost = 100 and profit markup = 15%, then profit = 15 and price = 115

% wastage

- If a finished qty of work of 100 requires a material qty of 120. The qty wasted is 20.

- Should the wastage be 20/100 = 20% or 20/120 = 16.67%?

- Both can be correct depending on which is used as the base.

- However, in pricing, when the payment is based on the finished qty, the qty wasted should be borne by the finished qty.

- In the above example, the addition to cover the qty wasted is 20/100 = 20%, so the wastage should be 20%.

- If a 3 x 6 finished board requires a 4 x 8 uncut board, the wastage to be allowed is (4 x 8) / (3 x 6) - 1 = 32/18 - 1 = 77.78%.

- To conclude, the wastage to be allowed

= qty wasted / finished qty

= (qty used - finished qty) / finished qty

= (qty used / finished qty) - 1. - The denominator is the payable qty (finished qty).

% bulkage (excavation)

- How to allow for the extra volume to work on if payment is based on the volume before bulking?

- Bulkage or bulking factor = volume after bulking / volume before bulking.

- Volume after bulking = volume before bulking x bulkage.

- The addition to cover the extra volume is volume before bulking x bulkage. This should be simple.

- Refer to estimating reference books for the percentages, which are material properties.

% shrinkage (concrete, mortar, plaster, screed) or % compaction (soil backfilling)

- How to allow for shrinkage if payment is based on the quantity after shrinkage?

- If shrinkage = 20%, for each 100 qty, qty shrunk = 20, qty left = 80.

- The addition to cover the qty shrunk = 20/80 = 25%.

- If shrinkage = 30%, for each 100 qty, qty shrunk = 30, qty left = 70.

- The addition to cover the qty shrunk = 30/70 = 42.86%.

- If shrinkage = S%, then the addition factor = S/(100-S).

- The denominator is the payable qty (qty left).

- Refer to estimating reference books for the percentages, which are material properties.

All-in rates and unit of quantity

- All-in rate = all-in price / quantity.

- Not all the costs are directly proportional to the quantity of the work, it can be a combination of:

- Variable costs

- Fixed costs.

- Cost = f(weight) + f(volume) + f(area) + f(length) + f(number) + f(quality) + f(time) + f(others).

- When the total price of a work item is required to be broken down into quantity and rate, the unit of the quantity to be used should be one which represents the most cost significant variable.

- If there are more than one cost significant variable, then the work item should be broken down into more than one sub-item.

- It is usual and easier to estimate the cost of a bigger sample quantity of a work item first and divide the cost by the quantity to obtain the unit rate so that:

- Those costs not directly related to the quantity of the work item can be shared

- Wastage, laps, etc. which are not measured in the quantity can be allowed for.

Rate build-up (estimating from the first principle)

- Labour costs:

- Daily rates to include for:

- daily basic wage

- travelling and meal allowances

- allowances for hand tools and personal accessories

- allowances for holidays with pay

- mandatory provident fund (MPF) contribution

- year end bonus

- incentive payments

- levies and insurances if not priced separately

- etc.

- Time to consider:

- taking from stores, hoisting, lowering

- placing, fixing

- non-productive travelling and recess time

- etc.

- Daily rates to include for:

- Material costs:

- Rates to include for:

- ex-factory costs, package

- export transportation, transit insurance

- customs clearance and duties

- demurrage, off-site storage

- local delivery

- off-loading, returning package

- etc.

- Quantities to consider:

- basic quantities

- breakage, damage, theft

- wastage (cutting, conversion)

- unmeasured laps

- bulkage, consolidation, shrinkage

- etc.

- Rates to include for:

- Plant costs (called "Equipment costs" in civil engineering contracts):

- Rates to include:

- Use of plant (not purchasing of plant)

- Mobilization, relocation and demobilization costs, if not measured separately

- Fuels and consumables

- Maintenance and repair.

- Time to consider:

- Time used

- Unavoidable idling time

- Mobilization, relocation and demobilization time, if not measured separately.

- Rates to include:

- Site and project overheads

- Expenses on site or off-site specifically due to the project, not specifically related to any particular group of work but are commonly shared.

- Head Office Overheads

- Expenses in running the head office, shared between different concurrent projects.

- Profit

- The expected profit with allowance for risks.

- Tax if charged based on total price (not in Hong Kong which implements profits tax on the realisable profit annually, not value added tax on turnover).

- Rates build-up applicable to measured work as well as preliminaries.

Cost Geometry

Cost vs quantity

Not a straight-line relationship between costs and quantities

- Cost = f(weight) + f(volume) + f(area) + f(length) + f(number) + f(quality) + f(time) + f(others).

- But, the pricing unit of an item of work or material is based on one kind of unit of measurement.

- This means that all other costs not related to that unit have to be converted to use that unit as the base.

- These other cost factors do not change in direct proportion to the pricing unit.

Total cost vs quantity

- The total cost of factory production (and therefore sales of materials and goods) does not increase in proportion to the increase in the quantity produced, since there are some initial fixed costs (e.g. factory, equipment, rental deposits) and recurring fixed costs (e.g. monthly rents, additional equipment when the existing capacity is exceeded) not in proportion to the quantity to be included.

- The total sales value may also not increase in proportion to the increase in the quantity sold (e.g. bulk discount, delivery vehicle not used to full capacity).

- The total cost is usually higher than the total sales value initially, but the total sales value must rise up to exceed the total cost eventually for the business to be viable.

Impact on unit cost and unit rate

- Making a unit rate competitive enough to secure sales volume and produce profit is important.

- Works or sales contracts usually require the unit rates to be fixed even though the quantities may be varied. If the variation is significant, there can be a huge loss or profit. Some contracts permit the adjustment of the unit rates in case of unexpected big changes.

- The quantity of any item of work can vary between different construction projects and how to estimate an appropriate unit rate is crucial.

Breakdown into more or less items

- It would be more expedient if less items need to be measured to arrive at the total cost or price.

- This means that the unit rate has to allow for the costs of other related items not measured separately.

- However, when the costs of other related items do not vary in proportion to the quantity of the item measured, the unit cost of the item measured would change significant to become unrealistic, then such other related items should be measured separately for costing.

- Therefore, the unit rates should only be required to include for related items which change in proportion to the quantity measured or for non cost significant ancillary items. Yet, significant changes to the quantity may still make the non cost significant ancillary items to become significant. This is an area for contractual claims.

Building form and shape

- Appreciate the effect of different site areas for the same building:

- Appreciate the effect of doubling the number of storeys:

- Appreciate the effect of elongating the building without increasing the floor area:

- Unit cost per floor area:

- Construction costs are usually compared based on unit cost per floor area.

- The above suggests that the unit cost per floor area cannot be a constant for the same type of buildings of different forms and shapes.

- Impact on design:

- The relationship of number, length, area and volume is more important for the design of the building form and shape.

- Whether a building is more economical or expensive than the other for the same floor area and type would primarily depend on the ratios of the numbers, lengths, areas and volumes of the building components to the floor areas, and then on the materials and standards.

Most significant cost parameters

- Appreciate which cost portions should bear more direct proportions to each parameter:

瞭解那部份的成本內容與那個造價參數有較直接的比例關係:-

- Parameters:

- Floor area (above ground + below ground)

樓面面積 - Ground area (= roof area)

地面面積 (=屋面面積) - Transfer structure area

轉換結構面積 - External elevation area

外立面面積 - Basement screen wall area or more effectively basement volume of excavation

地下室外牆面積或較有效的地下室土方體積 - Site area

工地面積 - External area (site area - ground area)

室外面積 - Number of equipment

台數 - Refrigeration tonnage

冷噸 - Other elemental quantities.

其他功能分部工程量。

- Floor area (above ground + below ground)

- Quick cost estimating:

- Using this small number of cost parameters can enable quick cost estimating.

- Accurate measurement:

- The values (quantities) of those parameters which will be used extensively throughout a cost estimate should be accurately measured, unlike the general message here that the cost estimates should be approximate.

Cost Factors

Generally

- Cost factors may be asked from different perspectives at different stages:

- Feasibility study before choosing site:

- What type of development?

- Which country and place to invest and develop?

- Why cost differently between countries, places and sites?

- Planning and design after fixing site:

- What design, provisions, types, standards of the whole and its components?

- Why cost differently?

- Tendering:

- Why tender prices so different?

- Construction:

- Why original contract sum changes?

- Feasibility study before choosing site:

- Cost factors generally:

- Some factors affect the quantities, and therefore the total cost.

- Some factors affect the unit cost per area or unit cost per length (e.g., roads, rails, tunnels, bridges, etc.).

- Some factors affect the unit rate per quantity of work.

- Price changes during the post contract stage are excluded here.

- Think and brainstorm:

- The factors can equally apply to other industries or commercial or even social sectors.

- Common sense knowledge is to be applied.

- Classify systematically:

- There is no absolute answer to "which classification is the best?".

- A systematic classification should help people think further systematically in the future and present the more relevant factors systematically depending on the perspective and stage.

No fixed prices

- One important thing to learn is that there is no fixed (constant) set of unit prices in any economy, as evidenced by the many factors suggested.

- Free market economies operate on free market competition of the prices. They would only regulate prices for using government services and some public utility services.

- The mainland, China used to fix a constant set of unit prices (by issuing standard price books) with moderate periodic inflationary adjustments but when foreign materials and equipment using foreign currencies are involved, the price fluctuations can become serious. After opening up the market, the mainland has admitted significant free market competition though some measures to regulate the prices are still implemented.

- Hong Kong operates as a free market economy. Therefore, there is no fixed set of unit prices for construction works. An exception to this is that Hong Kong Government publishes Schedule of Rates for term contract works. See notes at the end.

Reasons for variances in unit rates in the same city

- Even for work items of the same description, the rates can be quite different between projects due to various reasons.

- Design:

- Functions

- Materials and construction

- Standard.

- Site location:

- Transportation

- Restrictions.

- Construction:

- Project size

- Extent of mechanization

- Extent of standardization

- Extent of repetition

- Extent of pre-fabrication

- Volume of bulk purchasing

- Workmanship

- Weather

- Extent of safety measures

- Extent of environmental protection measures.

- Economic environment:

- Level of market competition

- Exchange rates

- Time differences.

- Contractual:

- Degree of contractual risks

- Harshness of contract terms

- Payment terms

- Degree of design liability and statutory submission obligations

- Extent of warranties.

- Human factors:

- Consultants’ attitude

- Owners and occupiers’ attitude and co-operation

- Tenderers’ pricing strategy in distributing the costs, profit and overheads differently across different work sections.

Country (assuming putting a done design to a different country)

- Different planning and design regulations.

- Different environmental requirements.

- Different tax requirements.

- Planned economy or free market economy.

- Significance of government intervention.

- Different purchasing power of local currencies.

- Availability of foreign currencies.

- Availability of local supply of labour, materials, plant and management.

- Degree of reliance on foreign supply of labour, materials, plant and management.

- Different requirements on holidays and restriction on working hours.

- Different productivity of local labour.

- Different extent of availability of public roads and utilities.

- Different degree of ease of evacuation of existing occupiers.

- Significance of corruption.

Site location and conditions

- Extreme climatic conditions: hot, cold, frozen work period, typhoon.

- Seismic zones.

- Existing status of use: greenfield or brownfield.

- Existing type of use: urban, rural or agricultural.

- Existing site topography: flat, hilly, mountainous, offshore, etc.

- Ground conditions: soft, rocky, reclaimed, submerged, swampy.

- Obstructions underground and above-ground.

- Availability of public roads and utilities.

- Ease of evacuation of existing occupiers.

- Congested site or sufficient space for storage and maneuvering.

Planning and design

- Functional type of the building or civil engineering construction.

- Class and standard of the construction.

- Planning and design regulations for different sites and constructions.

- Environmental requirements.

- Structural form of the construction (brick, reinforced concrete, steel, timber, composite).

- Plan shape of the construction. (Different elevation area to floor area ratios. Square building costs less than rectangular building on external elevations.)

- Storey height. (Storey height will affect the vertical elements of the building both internally and externally. Higher storey height will increase the volume of the building to be heated or cooled, and therefore HVAC services.)

- Number of storeys. (Different shares of the roof and ground slab and beam costs. Need to have staircases for non-single storey buildings. Need to have lifts and refuge floors for tall buildings.)

- Height of the construction. (Heavier loading on taller buildings.)

- Orientation of the construction. (Thermal transmission on external surfaces. Use of sunlight.)

- Impact on neighbouring properties.

- Extent of provision of construction components.

- Functions, materials and quality of components.

- Extent of site works and external works shared by the main construction (affecting unit cost per area or length).

Economic environment

- Stability of economy.

- Forecast of cost fluctuations.

- Level of market competition.

- Exchange rates and their changes.

- Time differences (if compared between projects at different times).

Construction

- Project size.

- Period of construction and its reasonableness.

- Ease of transportation.

- Access restrictions.

- Changing labour, material and plant costs over time.

- Extent of plant required and availability of plant.

- Availability of supervisory staff.

- Extent of hoardings, covered walkways, scaffolding required.

- Extent of temporary works required.

- Extent of safety measures required during construction.

- Extent of environmental protection measures required during construction.

- Extent of mechanisation.

- Extent of standardisation.

- Extent of repetition.

- Extent of pre-fabrication.

- Volume of bulk purchasing.

- Workmanship expected.

- Weather which may be encountered.

- Availability of temporary water and electricity.

- Risks of safety, health, environmental hazards.

- Risks of changing government policies and neighbourhood and social expectations.

Contractual

- Procurement method.

- Degree of contractual risks.

- Harshness of contract terms.

- Payment terms.

- Degree of design liability and statutory submission obligations.

- Extent of insurances, bonds and warranties.

Tenderers' ability and perception (causing differences in tender rates)

- Labour, material and sub-contract costs which can be sourced at the time of tendering.

- Availability of plant.

- Availability of supervisory staff.

- Availability of expertise.

- Availability of sufficient cash flow or reliance on loans.

- Reasonableness of the period of construction.

- Consultants’ attitude.

- Owners and occupiers’ attitude and co-operation.

- Tenderers' profit expectations.

- Tenderers’ pricing strategy in distributing the costs, profit and overheads differently across different work sections.

How about modular integrated construction?

- Designers’ capabilities.

- Statutory requirements.

- Factory capabilities.

- Early involvement of contractors.

- Off-site costs, delivery and logistics, factory’s environmental impact.

- On-site storage, hoisting, special jointing, fixings, weatherproofing, fire-resistance.

- Shortened period of site overheads.

- Local environment impact.

- Local workers’ prospect.

Consultants' Cost Data

Price information

- Build-up a database.

- Collect directive circulars and prices published by Government and authorities.

- Collect market prices from other commercial sources (e.g., cost software vendors).

- View newspapers, periodicals, internet.

- Enquire market prices from prospective contractors, sub-contractors and suppliers.

- Collate internal information.

- Analyse content ratios and unit costs of past projects.

- Obtain through tendering.

Consultants' source of data

- Tenderers when tendering will get their cost data by making enquiries with their prospective sub-contractors and suppliers.

- Consultants may make enquiries with prospective contractors, sub-contractors and suppliers for cost data but may only be able to obtain some indicative budgetary prices which may differ from that obtained under circumstances of real business opportunity and competitive tendering.

- To evaluate whether tender prices received are reasonable market rates, other cost data not received for the same tender would need to be used to compare.

- Consultants would therefore rely more on past cost data for cost estimating and for evaluation of tenders.

- Consultants would know the rates and prices in tenders received but would not normally know the costs, profit and overheads in the tenders. It does not really matter when the Consultants are interested more on the all-in rates. The details of costs, profit and overheads are only essential when handling claims.

- When estimating composite rates covering more than one work item, the quantity ratios of the constituent work items would be important.

- Rates:

- Tender prices (average of the lowest three shortlisted tenders)

- Final Account prices

- New inquiries (contractors, sub-contractors, suppliers)

- Architectural Services Department Schedule of Rates for Term Contracts for Building Works 2019 Edition:

- Architectural Services Department Schedule of Rates for Term Contracts for Building Works 2023 Edition:

- Builder's Works - https://www.archsd.gov.hk/media/publications-publicity/schedule-of-rates/sor2023_vol_1_bw_.pdf

- Corrigendum No. 1 - https://www.archsd.gov.hk/media/publications-publicity/schedule-of-rates/sor2023_corrigendum_no._1_%28Vol.1%29.pdf

- Building Services Works - https://www.archsd.gov.hk/media/publications-publicity/schedule-of-rates/sor2023_vol_2_bs_.pdf

- Corrigendum No. 1 - https://www.archsd.gov.hk/media/publications-publicity/schedule-of-rates/sor2023_corrigendum_no._1_%28Vol.2%29.pdf

- They are published once every many years and should be used with extreme caution for new works. The Contractor's percentage mark-ups on these rates should also be considered.

- Urban Renewal Authority Building Rehabilitation Platform - Reference Unit Rate - https://brplatform.org.hk/en/cost-reference-centre/reference-unit-rate.

- Quantity factors and ratios:

- Cost Analyses of Other Projects

- Analyses by sampling.

Adjust for time differences

- There can be up or down fluctuations of costs and prices over time. When using past cost data for the present or future work, adjustments should be made for the time differences.

- Indices for adjusting for time differences:

- Cost indices – reflecting labour and material costs

- Tender price indices – reflecting prices of work

- Consumer price indices – reflecting general consumer prices not just for the construction industry.

- Cost indices and tender price indices can change at different rates. Cost indices can rise but tender price indices may fall in case of severe competitive market lacking work.

Index references

- Census and Statistics Department - Index Numbers of the Costs of Labour and Materials used in Public Sector Construction Projects

- Census and Statistic Department - Average Wholesale Prices of Selected Building Materials

- Architectural Services Department - Building Works Tender Price Index

- Architectural Services Department - Building Services Tender Price Index

- Rider Levett Bucknall Construction Cost Update Hong Kong

- Arcadis Quarterly Construction Cost Review Hong Kong and China

Pre-Contract Cost Management and Control

Pre-contract cost management

- Principal cost management tasks during the pre-contract stage:

- Prepare cost estimates or cost plans

- Prepare cash flow tables

- Attend design meetings

- Monitor the design

- Adjust the cost estimates and reconcile

- Compare alternatives.

- Estimate, plan, update and control.

Need for pre-contract cost estimates for new works

- Know the costs for investment decisions:

- Calculate land bid price

- Calculate acceptable rental

- Evaluate the feasibility of the investment.

- Establish a project (development) budget.

- Obtain funding.

- Borrow money from the bank.

- Formulate a design brief which defines the scope and standard of the project.

- Monitor the design development to control the costs within budget.

- Estimate fees or review fee percentage.

Need for pre-contract cost estimates for renovation works

- Obtain consensus to renovate.

- Create a priced shopping list for selection.

- Establish a project budget.

- Obtain funding.

- Collect fund contributions (in case of joint ownership such as incorporated owners).

- Monitor the design development to control the costs within budget.

- Serve as the checklist for actual renovation work for tenders and final accounts (strictly following the approved list for public funded projects).

Best time to plan and control the costs

- As early as possible.

- Better chances to make design changes to find a better solution.

- To reduce abortive design costs and time.

Prepare Pre-Contract Cost Estimates

Ways to calculate cost estimates

- Techniques:

- Estimates should be done using expedient methods, approximations and shortcuts to reduce estimating time and costs in order to afford more estimates.

- Methods:

- By unit cost per floor area / length / number estimates

- By measuring the most significant cost parameters

- By measuring elemental quantities

- By measuring approximate quantities

- By pricing the bills of quantities or schedule of rates / works ready for issuance or already issued for tendering.

Estimating mottos 四字真言

- From big to small. 由大到小。

- From rough to fine. 從粗到細。

- Focus on the important. 重點出擊。

- Make bold assumptions. 大膽假設。

- Verify carefully. 小心求証。

- Compare with the unlike. 觸類旁通。

- Conduct self-checking. 自我覆核。

- Reconcile with the previous. 瞻前顧後。

- Empathize with the Client. 設身處地。

Different names of pre-construction cost estimates

- Rough Indication of Costs ("RIC").

- Preliminary Indication of Costs.

- Preliminary Cost Estimates.

- Elemental Cost Estimates.

- Cost Plans.

- Cost Models (An American term).

- Pre-tender Estimates.

Budgets, cost estimates and cost plans

- Budget:

- A budget is the maximum sum a Developer / Client is willing and able to spend on a project.

- Cost estimate:

- A cost estimate is a forecast of the probable ultimate cost based on the current design.

- It is required to be done throughout the pre-construction stages as well as the construction stage until the estimated costs become fixed prices.

- A cost estimate for now, if satisfactory and approved, will become the cost plan for the future design.

- Cost plan:

- A cost plan is a detailed cost framework for controlling future design.

- It sets out the portions of the total budget allocated to different parts of the construction so as to serve as the cost limits to the relevant parts of the construction.

- It may just be based on some interpolation from the cost data of other projects or may be based on some detailed cost estimate specifically prepared for the relevant design.

- It usually refers to the cost plan before the award of the principal contract. After that, the cost plan will be replaced with regular final statements.

- Rough indication of costs ("RIC"):

- It is a kind of cost estimates. It may be just based on unit cost / number or unit cost / floor area or unit cost / other functional unit to be used in the feasibility study or early design stage based on some ideas or sketch designs

- HK ArchSD still calls it "Rough Indication of Costs" when the estimate is still in the early stage though the details may be more than just based on unit cost per floor areas.

- Approximate estimate:

- Approximate estimates should be done using expedient methods, approximations and shortcuts to reduce estimating time and costs in order to afford more estimates.

- This principle should be applied to pre-construction cost estimates or post contract cost estimates.

- Detailed cost estimate:

- It is a more detailed cost estimate prepared when the design is more developed.

- "Detailed" refers to the number of items measured, rather than to the accuracies of the quantities estimated.

- Some consultants call it "Preliminary Cost Estimate", and some call it "Cost Plan".

- It may become the Budgetary Estimate if approved.

- Pre-tender estimate:

- A pre-tender estimate is no longer an approximate estimate and is prepared by pricing the bills of quantities ready for issuance or already issued for tendering.

- A logical sequence is like this:

- Rough Indication of Costs => Detailed Cost Estimate => Cost Plan / Budgetary Estimate => Pre-tender Estimate.

Elemental cost classifications

- Trade by trade classifications:

- Pricing documents for tendering are usually arranged in trade by trade or works section orders or work breakdown structures according to the local standard method of measurement or local practice.

- Elemental cost classifications:

- Instead of following the same order, pre-construction cost estimating in many countries (not all) adopt an elemental cost classification, which divides the costs of a construction project into various parts ("elements") each serving a specific function or common purpose such that the costs of alternatives serving the same function or purpose can be compared, evaluated and selected irrespective of their trades, works sections, design, specification, materials or construction.

- Classifying the costs of a building (or other construction) into elements would facilitate:

- Comparison of the costs of different design options serving the same elemental function

- Comparison with costs of other projects by elements

- Rationalizing the budget allocation between different elements for better use

- Quicker estimating based on elemental quantities which are easier to measure

- Analysis of data for different projects on the same basis and classification.

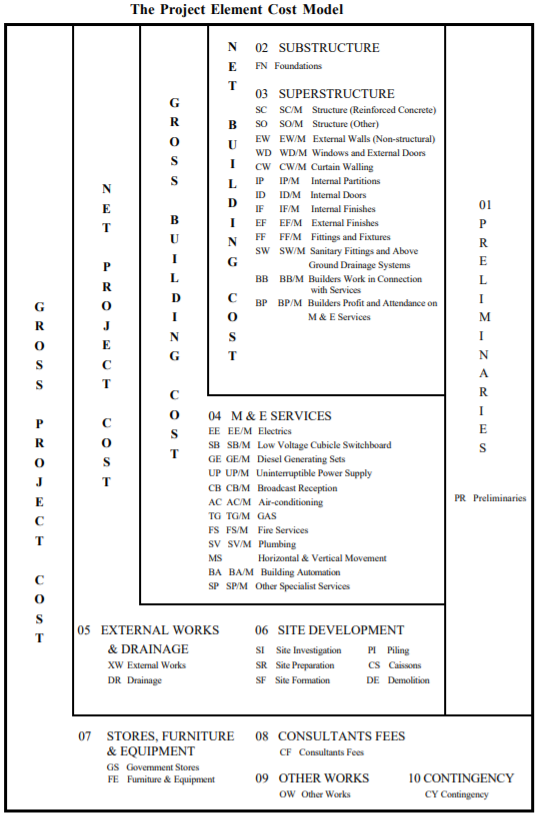

- Different elemental cost classifications in Hong Kong:

- Different QS practices and ArchSD have different elemental classifications.

- ArchSD adopts the following Project Element Cost Model as described in the Standard Method of Measurement for Building Elements 2020 Edition published by the Architectural Services Department (https://www.archsd.gov.hk/media/publications-publicity/schedule-of-rates/asdsmmbe_2020.pdf):

- Many other places outside Hong Kong also have their own elemental cost classification systems, e.g.:

- UK's Uniclass:

- https://en.wikipedia.org/wiki/Uniclass#The_tables

- https://www.thenbs.com/our-tools/uniclass-2015#classificationtables(browse the Element / Function table)

- UK RICS's NRM 1 ("New Rules of Measurement 1: Order of cost estimating and cost planning for capital building works"):

- USA's Omniclass:

- https://www.csiresources.org/standards/omniclass (incorporating MasterFormat for Work Results and UnitFormat for Elements)

- Australia, Canada, Malaysia, Nigeria, etc.

- UK's Uniclass:

- ICMS:

- International Cost Management Standard (ICMS) (https://icms-coalition.org/the-standard/) is a global classification and reporting standard covering the life cycle costs and carbon emissions of building and civil engineering projects. "elements" is called “Groups” and “Sub-Groups” in ICMS 3 so that they are equally applicable to costs and carbon emissions. The examples shown here are based on that standard. See also International Cost Management Standard.

Construction floor area and gross floor area in Hong Kong

- Different areas:

- For costing, leasing and sales of buildings and related land, people usually have to refer to unit cost or price per floor area of the buildings as the most important controlling parameter.

- However, there are many types of floor areas being defined for different purposes in Hong Kong or other places outside Hong Kong. An understanding of their possible differences is important.

- CFA:

- Quantity Surveyors measure the construction floor area (CFA) in order to estimate the total construction cost of a building.

- GFA:

- Lands leased by the Government in Hong Kong are subject to limitation on the gross floor areas (lease GFA) of the buildings which may be built on the land. Some of the construction floor area is not accountable for the lease GFA. The Lands Department is responsible for the control. Read the Lands Department's Practice Note on Accountable and Non-Accountable GFA under Lease at https://www.landsd.gov.hk/en/images/doc/1998_1A_text.pdf.

- Building plans have to be submitted to the Buildings Department for approval and consent before construction. The gross floor areas (GFA) are also controlled by the Buildings Regulations. Read the Buildings Department's Practice Note on Calculation of Gross Floor Area and Non-accountable Gross Floor Area at https://www.bd.gov.hk/doc/en/resources/codes-and-references/practice-notes-and-circular-letters/pnap/APP/APP002.pdf.

- The Lands Department's Practice Note says while the Lands Department is usually prepared to follow the Buildings Department's ruling in exemptions from GFA calculations, it reserves its right and absolute discretion to do otherwise in individual cases.

- Saleable area:

- There are further complications due to the use of saleable area for residential properties. See Cap. 621 Residential Properties (First-hand Sales) Ordinance at https://www.elegislation.gov.hk/hk/cap621.

International Property Measurement Standards (IPMS)

- The International Property Measurement Standards at https://ipmsc.org/standards/ are intended to unify the rules of measurement of various kinds of floor areas for different types of buildings.

- A single harmonised standard covering All Buildings has been published on 15 January 2023 to supersede all previously published standards for individual asset classes.

- IPMS 1 (gross external floor area) and IPMS 2 (gross internal floor area) are referred to by ICMS.

- Read this and appreciate the diagrammatic illustration.

- CFA in Hong Kong is close to IPMS 1 with one exception: accessible rooftop terraces are included in IPMS 1 but not in Hong Kong CFA.

Need for historical cost analyses

- Before talking about the cost estimates, it may be appropriate to talk about cost analyses first.

- Cost analyses are needed to:

- Benchmark new projects

- Provide cost data for new estimates

- Provide cost parameters for new estimates.

Cost analysis example adopting ICMS

- Analyse the awarded or final prices of a project.

- Re-classify the costs into line items following the same classification used for the cost estimates or cost plans.

- Identify elemental quantity for each line item - the quantity can best represent the cost changes in case of quantity changes of that line item.

- Divide the cost of each line item by its elemental quantity to give a single all-inclusive rate (elemental unit rate).

- The elemental unit rates are very useful when the cost of a new project is required to be estimated before any detailed design is available.

Apply the elemental unit rates to new projects

- Elemental quantities can be measured for the new project and priced at elemental unit rates of the reference projects.

- There are not too many items of elemental quantities to be measured. The cost estimating process can therefore be very fast.

- Of course, the elemental unit rates may not be directly applicable to the new project.

- It should at least be adjusted for the changes in the price levels from the times it was applicable to the reference project to the time of the new project, and then for other changed factors.

Get quantity ratios or factors

- A cost analysis should also contains quantity ratios or factors such as:

- elevation area : floor area

- concrete volume per floor area

- formwork area per concrete volume or floor area

- rebar weight per concrete volume or floor area

- etc.

- These quantity ratios can serve as useful references when estimating the costs of new projects.

- Apart from using the data in a cost analysis to estimate the cost of a new project in the absence of detailed design, the data can also be used to benchmark the cost of a new project after a more detailed cost estimate is done to ensure that the new project would not go out of order.

- Hong Kong Government uses this technique to control the costs of new project at the design stage.

- The Architectural Services Department has published a very detailed Project Cost Analysis Form.

Changes in cost and price levels

- Due to changes in the market conditions, the unit rates for exactly the same description of work may change over time.

- The market conditions may include fluctuations in the costs of labour, materials and plant, market competition, and other factors.

- Unit rates applicable in the past would need to be adjusted to the current level.

- Tender price or cost indices are therefore prepared to provide the adjustment factors.

- Their differences should be appreciated.

- Tender price indices and cost indices can fluctuate at different rates because price = cost + profit, and the price may increase less than the cost increase in order to secure projects or may increase more in case the market is full.

Different methods of approximate cost estimating

- Unit method (common).

- Superficial method or area method (common).

- Cubic method (seldom used for buildings).

- Storey enclosure method (seldom used now).

- Elemental cost estimates (common):

- Elemental quantity method

- Approximate quantity method.

- Condensed elemental method using the most significant cost parameters.

Pre-tender estimate:

- A pre-tender estimate is no longer an approximate cost estimate and is prepared by pricing the bills of quantities ready for issuance or already issued for tendering.

Unit method

- The estimated cost of a building is calculated based on the number of functional units provided by the building x unit cost per functional unit.

- ICMS has suggested the following functional units for buildings: number of occupants | number of bedrooms | number of hospital beds | number of hotel rooms | number of car parking spaces | number of classrooms | number of students | number of passengers | number of boarding gates.

- The unit method is a crude method serving as an early indication of the probable order of cost of the average building of the relevant type.

- It is not useful for forecasting with a high degree of accuracy the costs of newly proposed buildings of the same type because their designs can be very different.

- However, it may be used by clients and in particular government departments to serve as a cost yardstick controlling the budget of newly proposed projects.

- It is still also useful to serve a check that a unit cost per floor area may sound reasonable but, when expressed in unit cost per functional unit, the unit cost can be out of order because of excessive floor area per functional unit.

Superficial method or area method

- The estimated cost of a building is calculated based on the floor area of the building x unit cost per floor area.

- This is the most commonly used method, possibly because the sales and rental prices are also expressed in unit cost per floor area.

- Note however that there are many definitions of "floor area". The same definition should be consistently applied.

Cubic method (seldom used for buildings)

- The estimated cost of a building is calculated based on the volume of the building x unit cost per volume.

- In theory, the volume can take care of the different storey heights of the building.

- This is not commonly used probably because the floor areas are more readily available, and calculating the volumes would mean a further step to be done.

- The cubic method may be useful for site formation works or civil engineering works involving massive volume of work.

Storey enclosure method (seldom used now)

- In essence, the estimated cost of a building is calculated based on the total of the weighted areas of bottom slabs (basement or ground), suspended floor slabs, roof slabs, and walls below and above ground x unit cost per total weighted area.

- Each type of slabs or walls are given different fixed weightings to reflect their relative ratios of costs.

- The calculation is much more complicated than the superficial method or the cubic method.

- With so many varieties of construction components and materials, whether the fixed weightings can truly reflect the relative ratios of costs is doubtful.

- This method is seldom used these days.

- Search the internet for details and examples.

Elemental quantity method

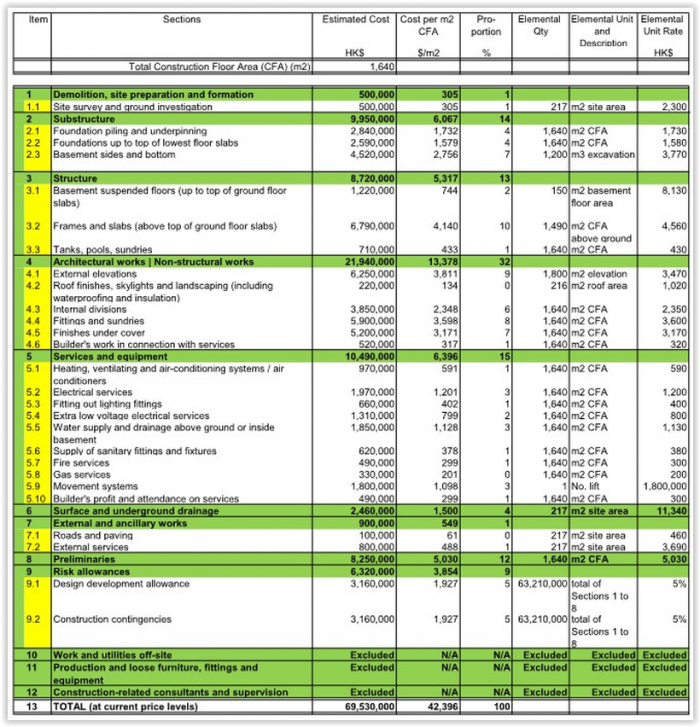

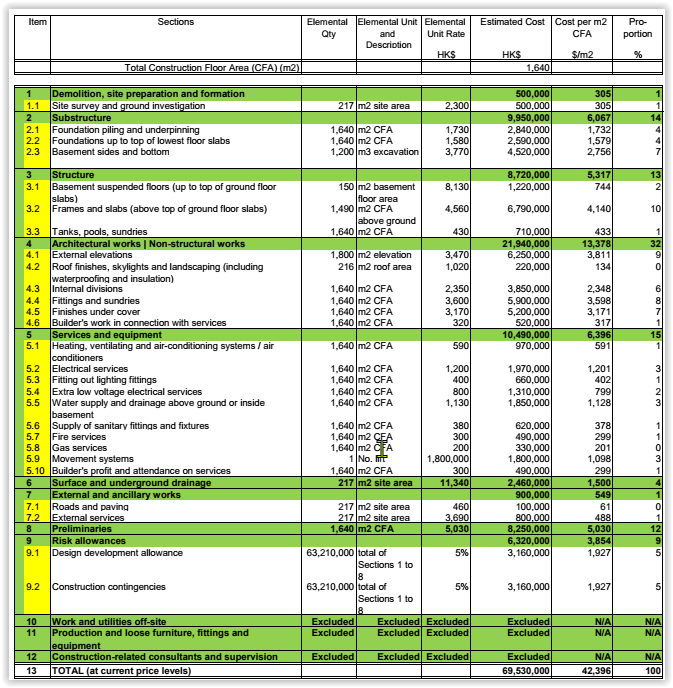

- The building cost is classified into different elements (or Groups or Sub-Groups as used in ICMS as shown under the "Sections" column in the example below which follows ICMS classifications).

- Each element is represented by an appropriate elemental quantity which best represents the elemental cost (i.e., changing proportionally).

- It can be seen from the example below that the elemental quantities generally adopt the values of the most significant cost parameters discussed below.

- The estimated cost of a building is calculated based on the total of (elemental quantity x elemental unit rate).

- It takes into account the different forms, provisions and standard of the proposed new building better than the average unit cost per floor area.

- It is therefore a more accurate method than the superficial method.

- However, while the elemental quantities are simple to measure, the elemental unit rates would rely on reliable cost data from other projects or may need careful build-ups.

- This method should only be used at the early stage of design.

- At the time of the elemental quantity cost estimates, there would not be much details to measure approximate quantities and one has to rely on past cost analyses or some estimated quantity factors and ratios to estimate the elemental unit rates.

- The elemental unit rates, quantity factors and ratios should be critically reviewed to see whether they should remain unchanged or adjusted when the design of the building is changed even though the elemental quantities can remain unchanged.

- The price levels of past projects must be adjusted to the present day for use.

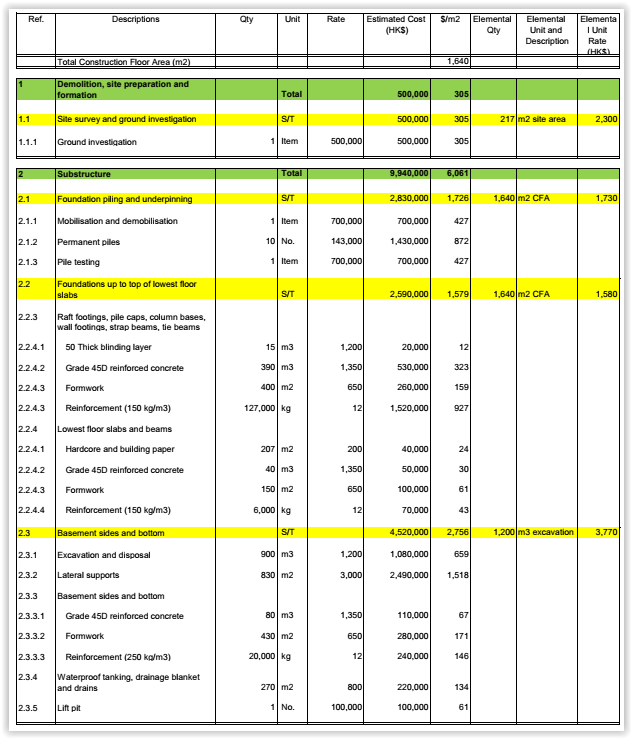

Approximate quantity method

- The estimated cost of a building is calculated based on the total of (approximate quantity of major item of work x unit rate per quantity of major item of work inclusive of costs of minor items):

- It does not usually show the elemental quantities and elemental unit rates just to save time.

- As the design is more developed, it is possible to measure the work constituting the building more accurately and apply more appropriate unit rates relevant to the materials and standard chosen.

- The quantities are approximate to reduce the time to measure so that a quicker cost estimate can be produced to reflect the updated cost of the design and enable any subsequent measures to control any unexpected costly design.

Condensed elemental method using the most significant cost parameters

- Users of the elemental quantity method may find that many elemental quantities are the same for different elements and can in fact be reduced into a few most significant cost parameters:

- Floor area (above ground + below ground)

- Ground area (= roof area)

- Transfer structure area

- External elevation area

- Basement screen wall area or more effectively basement volume of excavation

- Site area

- External area (site area - ground area)

- Number of equipment

- Refrigeration tonnage

- Other elemental quantities.

- The estimated cost of a building is calculated based on the total of (quantity of the above cost parameter x composite unit rate per quantity of cost parameter).

- This can provide a quick and equally reliable cost estimate though not as detailed as the elemental quantity cost estimate.

- For renovation works, the following may be used:

- External elevation area

- Roof area

- Main entrance lobby area

- Upper floor lobby area

- Staircase area

- Number of plumbing and drainage main stacks

- Number of kitchens and bathrooms

- Number of water supply outlets and drainage outlets (including those at roof and plant rooms).

Contents of cost estimates

- Cover page:

- Estimate Number

- Project Name

- Project Location

- Estimate Date